In 1988, Gov. Michael Dukakis claimed the Democratic presidential nomination by also claiming credit for the "Massachusetts Miracle."

High-tech and financial service industries blossomed in the Boston area during the 1980s after the state had been decimated by a massive exodus of manufacturing.

Two decades later, another Massachusetts governor apparently hopes to ride another miracle to a presidential nomination. Gov. Mitt Romney, barely concealing his desire to be the Republican standard bearer in 2008, recently pulled off a remarkable political feat: orchestrating bipartisan support for enacting compulsory health coverage for all Bay State residents.

So far, nothing you didn’t already know.

They found a way to get to a major expansion of coverage that people could agree on.

But for some, universal coverage does not go far enough. They advocate government-funded health coverage for everyone

Government funded. Don’t you just love that term. Makes it sound like the government pays for things with their money. Of course the only problem is, the government doesn’t have their own money.

It is really OUR money.

There really is no such thing as government funded. The correct term is TAXPAYER funded.

We now return you to your regular reading.

This is particularly favored by healthcare providers weary of dealing with the middlemen that get between them and the patient

Didn’t we just establish that the government IS a middleman? And I have to wonder who these providers are. Is it the same ones who complain about the low reimbursement from taxpayer funded programs like Medicare & Medicaid? The same providers who have to see twice as many patients to make up for every one Medicare/Medicaid patient just to break even?

With or without the government, the nation's haves subsidize the healthcare of the have-nots. They do so with a combination of taxes, higher insurance payments and higher medical bills.

WOW! Someone actually “gets” it.

Healthcare providers absorbed about $35 billion in uncompensated care in 2003. But those costs are shifted to taxpayers who subsidize public hospitals, higher charges for those who pay their bills, and higher insurance premiums for businesses and their employees. Texas family health insurance premiums were $1,551 higher in 2005 because of uncompensated medical care, according to a 2005 Families USA study.

Someone is finally putting a face on the cost of the uninsured. But wait, there’s more!

Most of the uninsured in Massachusetts fell into three groups, the proportions of which are fairly typical nationwide:

About 20 percent were poor people who qualify for Medicaid but haven't bothered to sign up. This represents new spending for the state, but this group is entitled to a program.

About 40 percent are low-income households that don't qualify for Medicaid but cannot afford health insurance. The state will subsidize their premiums.

The remaining 40 percent were the primary target of the mandate. They can afford health insurance but simply choose not to buy it. When they are hit by catastrophic medical bills, they can't pay, so the rest of us have to pick up the tab.

Translation:

About 20% of the uninsured QUALIFY for taxpayer assisted care but fail to take advantage of an existing system that cost them little or NOTHING.

Another 40% of the uninsured CAN AFFORD coverage, but choose to shirk their responsibility as an adult and expect the rest of us to take care of them.

Something is terribly wrong with this picture.

Saturday, April 29, 2006

Blogging for MS - Thank You!

This morning, my lovely wife and daughter participated in the Walk for MS. This was their first year, and they did meet their goal. Actually, they went a little over!

Thank you to everyone who helped!

Friday, April 28, 2006

A Health Care Money Tree

Joe Kristan has a great take-down of a congresscritter's critique of HSA's. Interesting reading, because Joe (even though -- or maybe despite? -- the fact that he's a professional bean counter) "gets" the premise undergirding HSA's, and has understands the stakes. Highly recommended.

And while you're there, Joe does take comments...

Doughnut Hole

Mildred Lindley is stuck in a hole, the doughnut hole -- "right in the middle of it," she says -- that comes with Medicare's new prescription drug benefit.

Just four months into the program, Lindley has hit the point in her coverage where she has to pick up, at least for a few months, the full cost of the medication she takes to keep her bone marrow cancer in remission. As a result, her two-month supply of Thalomid shot up from $40 to a whopping $1,300.

One of the “side effects” of Medicare Part D prescription drug coverage.

"If I can't get it, I guess I'm here until the Lord takes me out. That's all I can do, because there's no way I can afford it," said Lindley, an 80-year-old from Jonesboro, Arkansas.

"I'm in the hole all right."

At least she has a sense of humor about it, but this is no laughing matter.

Under the standard drug benefit, the government subsidizes the drug costs for seniors and the disabled. But after costs reach $2,250, the subsidy stops until a beneficiary has paid out $3,600 of his or her own money. Then, the government will start picking up 95 percent of each purchase.

This is one of those can’t win situations. Before Part D there was no drug coverage.

After Part D this can happen . . .

However, there are beneficiaries who are convinced they will be worse off, many of whom had relied on free medicine provided by the drug manufacturers. They were told by the manufacturers this year that the free supplies would stop now that they were eligible for Medicare coverage.

Prescription assistance plans may go the way of the buggy whip.

Or maybe not?

A new opinion from the Inspector General of DHS gave approval to drug manufacturers to supply free medicine to low-income individuals who are not only eligible for Part D but also enrolled in a Medicare drug plan.

Either way, this is just another example of government meddling in something that is now worse than it was before.

Just four months into the program, Lindley has hit the point in her coverage where she has to pick up, at least for a few months, the full cost of the medication she takes to keep her bone marrow cancer in remission. As a result, her two-month supply of Thalomid shot up from $40 to a whopping $1,300.

One of the “side effects” of Medicare Part D prescription drug coverage.

"If I can't get it, I guess I'm here until the Lord takes me out. That's all I can do, because there's no way I can afford it," said Lindley, an 80-year-old from Jonesboro, Arkansas.

"I'm in the hole all right."

At least she has a sense of humor about it, but this is no laughing matter.

Under the standard drug benefit, the government subsidizes the drug costs for seniors and the disabled. But after costs reach $2,250, the subsidy stops until a beneficiary has paid out $3,600 of his or her own money. Then, the government will start picking up 95 percent of each purchase.

This is one of those can’t win situations. Before Part D there was no drug coverage.

After Part D this can happen . . .

However, there are beneficiaries who are convinced they will be worse off, many of whom had relied on free medicine provided by the drug manufacturers. They were told by the manufacturers this year that the free supplies would stop now that they were eligible for Medicare coverage.

Prescription assistance plans may go the way of the buggy whip.

Or maybe not?

A new opinion from the Inspector General of DHS gave approval to drug manufacturers to supply free medicine to low-income individuals who are not only eligible for Part D but also enrolled in a Medicare drug plan.

Either way, this is just another example of government meddling in something that is now worse than it was before.

Still Beating Your Wife?

So tell me, are you still beating your wife?

This not so funny line surfaced many years ago as an example of asking a question that makes you look bad no matter how you answer.

If you say “no”, that implies you did beat your wife but are no longer.

If you say “yes”, well, you know . . .

Now you can ask the big drug companies the same question, just phrased differently. “So tell me Pharma, are you still telling people they are sick just to sell your drugs?”

A lot of money can be made from healthy people who believe they are sick. Pharmaceutical companies sponsor diseases and promote them to prescribers and consumers

This particular practice of “inventing” disease has been a burr in my saddle for some time now. At one time we had heartburn. The treatment was to take an antacid and refrain from eating the food that caused the discomfort. Now we have medicines that allow us to eat freely of anything without experiencing the repercussions.

I am not a doctor, but something tells me if my body reacts negatively to a substance, perhaps I should listen to my body rather than some advertiser. It’s like the first puff on a cigarette; your body is trying to tell you this may not be good for you.

Some forms of medicalising ordinary life may now be better described as disease mongering: widening the boundaries of treatable illness in order to expand markets for those who sell and deliver treatments

It seems to me the author of this article is taking some liberties by creating words like “prescribers” and “medicalising” but I am not going to take issue with that because I do believe the underlying message needs to get out.

Within many disease categories informal alliances have emerged, comprising drug company staff, doctors, and consumer groups. Ostensibly engaged in raising public awareness about underdiagnosed and undertreated problems, these alliances tend to promote a view of their particular condition as widespread, serious, and treatable

No argument there. There is definitely a benefit to getting information about symptoms into the hands and minds of the public. This is good when you talk about early warning signs for cancer or heart condition. I have to question the purpose when the condition is a hair loss, an irritable bowel or yellow nails.

Around the time that Merck's hair growth drug finasteride (Propecia) was first approved in Australia, leading newspapers featured new information about the emotional trauma associated with hair loss.

Emotional trauma? Give me a break. You would think this is a male form of post-partum depression.

Irritable bowel syndrome has long been considered a common functional disorder . . . . . . What for many people is a mild functional disorder requiring little more than reassurance about its benign natural course is currently being reframed as a serious disease attracting a label and a drug, with all the associated harms and costs.

No doubt, DTC (direct to consumer) advertising has its’ place and it does produce positive results when a patient is encouraged to discuss symptoms of a REAL disease with their doctor. But some of the information is just going way too far.

And in case you are wondering, now that my hair is not falling out I am no longer beating my wife.

This not so funny line surfaced many years ago as an example of asking a question that makes you look bad no matter how you answer.

If you say “no”, that implies you did beat your wife but are no longer.

If you say “yes”, well, you know . . .

Now you can ask the big drug companies the same question, just phrased differently. “So tell me Pharma, are you still telling people they are sick just to sell your drugs?”

A lot of money can be made from healthy people who believe they are sick. Pharmaceutical companies sponsor diseases and promote them to prescribers and consumers

This particular practice of “inventing” disease has been a burr in my saddle for some time now. At one time we had heartburn. The treatment was to take an antacid and refrain from eating the food that caused the discomfort. Now we have medicines that allow us to eat freely of anything without experiencing the repercussions.

I am not a doctor, but something tells me if my body reacts negatively to a substance, perhaps I should listen to my body rather than some advertiser. It’s like the first puff on a cigarette; your body is trying to tell you this may not be good for you.

Some forms of medicalising ordinary life may now be better described as disease mongering: widening the boundaries of treatable illness in order to expand markets for those who sell and deliver treatments

It seems to me the author of this article is taking some liberties by creating words like “prescribers” and “medicalising” but I am not going to take issue with that because I do believe the underlying message needs to get out.

Within many disease categories informal alliances have emerged, comprising drug company staff, doctors, and consumer groups. Ostensibly engaged in raising public awareness about underdiagnosed and undertreated problems, these alliances tend to promote a view of their particular condition as widespread, serious, and treatable

No argument there. There is definitely a benefit to getting information about symptoms into the hands and minds of the public. This is good when you talk about early warning signs for cancer or heart condition. I have to question the purpose when the condition is a hair loss, an irritable bowel or yellow nails.

Around the time that Merck's hair growth drug finasteride (Propecia) was first approved in Australia, leading newspapers featured new information about the emotional trauma associated with hair loss.

Emotional trauma? Give me a break. You would think this is a male form of post-partum depression.

Irritable bowel syndrome has long been considered a common functional disorder . . .

No doubt, DTC (direct to consumer) advertising has its’ place and it does produce positive results when a patient is encouraged to discuss symptoms of a REAL disease with their doctor. But some of the information is just going way too far.

And in case you are wondering, now that my hair is not falling out I am no longer beating my wife.

Thursday, April 27, 2006

Blue News

Thirteen more lawsuits were filed Thursday in Los Angeles alleging that major health insurance companies illegally canceled policies for patients already approved for medical treatments.

According to the complaints, the insurers have created "retroaction review" departments whose sole purpose is to terminate policies for patients who had previously been given approval for medical treatments.

I will be interested in seeing how this plays out. I will also be surprised to see if this statement “departments whose sole purpose is to terminate policies for patients who had previously been given approval for medical treatments” holds up.

"We do not rescind coverage based on someone having a diagnosis or receiving services," he said. "We rescind based on misrepresentations in an application that we discover."

Misrepresentation on an application is just as much fraud as is misrepresentation by an agent selling coverage. Both are criminal acts.

After a patient files a claim, the insurance company re-examines the application to try to find any omissions or inconsistencies, he said.

Patients then get dumped for inconsistencies -- not fraud.

Isn’t an inconsistency in what is written on the application with what is reality a fraudulent act? Seems so to me.

Plaintiff Parvin Mottaghi of Glendale alleges she has $700,000 in bills after Blue Shield canceled her policy following an approved open-heart surgery by claiming the application was incomplete. She is now uninsured.

I am sure there is more to this story that has not been told. I could speculate, but that would make me no better than the reporter who authored this story and omitted pertinent facts.

Don't misread me. I do empathize with the individuals who have had their coverage cancelled, but I also am aware of the fraud that is committed against carriers with some regularity.

According to the complaints, the insurers have created "retroaction review" departments whose sole purpose is to terminate policies for patients who had previously been given approval for medical treatments.

I will be interested in seeing how this plays out. I will also be surprised to see if this statement “departments whose sole purpose is to terminate policies for patients who had previously been given approval for medical treatments” holds up.

"We do not rescind coverage based on someone having a diagnosis or receiving services," he said. "We rescind based on misrepresentations in an application that we discover."

Misrepresentation on an application is just as much fraud as is misrepresentation by an agent selling coverage. Both are criminal acts.

After a patient files a claim, the insurance company re-examines the application to try to find any omissions or inconsistencies, he said.

Patients then get dumped for inconsistencies -- not fraud.

Isn’t an inconsistency in what is written on the application with what is reality a fraudulent act? Seems so to me.

Plaintiff Parvin Mottaghi of Glendale alleges she has $700,000 in bills after Blue Shield canceled her policy following an approved open-heart surgery by claiming the application was incomplete. She is now uninsured.

I am sure there is more to this story that has not been told. I could speculate, but that would make me no better than the reporter who authored this story and omitted pertinent facts.

Don't misread me. I do empathize with the individuals who have had their coverage cancelled, but I also am aware of the fraud that is committed against carriers with some regularity.

Oleaginous Verbiage

In only 10 minutes, my patient had come to hate me, and who could blame her? I had frowned at her blood pressure, rolled my eyes at her weight, clucked at her blood sugar readings, asked some pointed questions about her drinking habits and pointed out the possible relationship between her chronic stomachaches and her tourniquet-tight jeans.

This must be why I don’t go to doctors.

First she just looked miserable and guilty, but by the time I got around to asking exactly what she had eaten for dinner the night before, she had become downright hostile. "Cheesecake," she spat out, with venom.

I am guessing there is a problem with this response. Cheesecake, being a dairy product, does not last forever even with good refrigeration. It’s either eat it or throw it out.

Under the circumstances, there was only one thing to say, and I didn't hesitate for a second. "By the way," I said, "I've been meaning to tell you, I love what you've done with your hair."

Somehow this approach doesn’t work with my wife. She still insists on returning to the insulting remark that got me in hot water to start.

We were taught to call them lubricating comments: little morsels of oleaginous verbiage tucked into the usual miserable catechism to ease it along a little.

Lubricating comments, huh? No, don’t think I will go there . . .

When does it all stop? I like your tie. You like my sense of humor. I appreciate your punctuality. You love my pen. Look, I'm sorry but I have run out of things to like about you, and I hate your cholesterol. Can we get back to work?

So much for the verbal foreplay, now it’s down to business.

Next!!

This must be why I don’t go to doctors.

First she just looked miserable and guilty, but by the time I got around to asking exactly what she had eaten for dinner the night before, she had become downright hostile. "Cheesecake," she spat out, with venom.

I am guessing there is a problem with this response. Cheesecake, being a dairy product, does not last forever even with good refrigeration. It’s either eat it or throw it out.

Under the circumstances, there was only one thing to say, and I didn't hesitate for a second. "By the way," I said, "I've been meaning to tell you, I love what you've done with your hair."

Somehow this approach doesn’t work with my wife. She still insists on returning to the insulting remark that got me in hot water to start.

We were taught to call them lubricating comments: little morsels of oleaginous verbiage tucked into the usual miserable catechism to ease it along a little.

Lubricating comments, huh? No, don’t think I will go there . . .

When does it all stop? I like your tie. You like my sense of humor. I appreciate your punctuality. You love my pen. Look, I'm sorry but I have run out of things to like about you, and I hate your cholesterol. Can we get back to work?

So much for the verbal foreplay, now it’s down to business.

Next!!

The Policy that Fell to Earth (Part One)

Universal Life insurance was developed in the early 80’s primarily as a response to money market accounts.

Hunh?

Okay, let’s rewind a little:

Back in the early 80’s interest rates were sky-high (20%+ mortgages, 17%+ money market “savings” accounts). Folks that owned whole life insurance policies saw a growth rate of 3-5%, and a loan interest rate of about 4-5%. A lot of these folks looked at their insurance policies, and did the math: I can borrow the funds for 5%, make 18%, and there’s essentially no risk.

Where do I sign up?!

Carriers were understandably less than sanguine about this, and looked for a way to staunch the flow. They knew that a lot of folks were intrigued by the “Buy Term and Invest the Difference” approach, and sought to capitalize on it. What emerged was a policy that stripped away many of the guarantees of whole life (WL), but offered the potential of greater growth. This was also the dawn of the modern computer age, which made it technologically possible for companies to illustrate more complex policies.

Thus was born Universal Life. It offered higher current interest rates than conventional WL plans, and a minimum guaranteed interest rate. The policy itself was really a hybrid: the cost of the insurance was, for the first time, “unbundled” from the plan, and one could see what the actual cost of the death benefit could be. And that cost could change from time to time, based on the insurance companies’ experience.

There is a current charge, and a guaranteed maximum charge.

It also offered more flexibility than its WL predecessor: one could change the premium, and the death benefit, pretty much at will. So if one came into some extra cash, one could dump it into the policy to give it a push; if one had a run of bad luck, one could lower (or even skip) the premiums.

Pretty cool, and a useful tool.

The problem is that we all assumed what has historically been the case: that over a given period of time (say, 20 years), interest rates always go up. That is, they go up and down, but the average interest rate for that 20 years will always be higher than the initial rate. By the way, I’m not pontificating here: I actually did the research early on in my career.

The problem is, for the past 10 or 15 years, this has not been the case, and the policies are beginning to “blow up.” That’s insurespeak for lose value, and threaten to lapse.

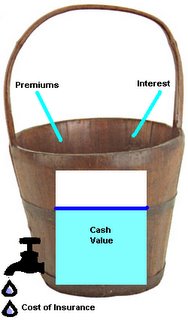

Think of the policy as a bucket:

At the top, we see Joe’s premiums going in, year after year. And we see the insurance company depositing interest each year.

In the middle, we see the cash value of the policy growing and growing (it’s comparable to the equity in your house).

At the bottom, there’s a spigot, draining out the cash value at a rate that’s determined primarily by the cost of the insurance (although loan interest would play a part, as well). In the early years, when Joe’s young, the spigot is opened just a little, so only a few drops leak out, and they’re more than compensated for by the premiums and the interest.

The goal is to keep enough “water” (cash value) in the bucket so that it doesn’t ever run dry.

Ok, so now what?

Well, for that, see Part 2…

Wednesday, April 26, 2006

This Just In . . .

Smoking isn't the problem; lack of health insurance is

Now there is a novel idea if I ever heard one.

Thousands of people are at increased risk for many conditions because they live in poverty, without adequate nutrition, or in an unhealthy environment? What good is a healthy workplace if you can't go home to a healthy household?.

Uh-huh. Sounds just a tad Socialistic, don’t you think?

The state claims to abhor smoking yet continues to generate huge sums of money through cigarette taxes and even plans to raise them?

This money is not being used to provide health care for people who need it? It's truly hypocritical not to.

Why is the Legislature focusing on trying to prevent speculative illnesses instead of helping people who need medical care right now

Use cigarette taxes to provide health care. Makes sense to me. How about extra taxes on double cheeseburgers to pay for health care? Next we can tax Halloween & Valentines candy.

I suggest the legislators get their heads out of their ashtrays and work on:

Passing legislation to ensure all citizens have access to adequate medical care and affordable health insurance.

How about legislated affordable housing, free loans for everyone. While we are at it, I wonder if the legislature could do something about my neighbors alarm that seems to go off in the middle of the night whenever he is out of town.

I propose refusing to obey this law until our legislators demonstrate they really care about our health by passing measures that provide access to health care to all.

Actually Anthony, some states have already told carriers they must accept anyone who applies, regardless of their health history. States like MA, NY, ME, NH & VT have all prohibited carriers from excluding people regardless of health. In doing so, they have also just about tripled the cost of health insurance.

This guy is going to make a great lawyer.

Now there is a novel idea if I ever heard one.

Thousands of people are at increased risk for many conditions because they live in poverty, without adequate nutrition, or in an unhealthy environment? What good is a healthy workplace if you can't go home to a healthy household?.

Uh-huh. Sounds just a tad Socialistic, don’t you think?

The state claims to abhor smoking yet continues to generate huge sums of money through cigarette taxes and even plans to raise them?

This money is not being used to provide health care for people who need it? It's truly hypocritical not to.

Why is the Legislature focusing on trying to prevent speculative illnesses instead of helping people who need medical care right now

Use cigarette taxes to provide health care. Makes sense to me. How about extra taxes on double cheeseburgers to pay for health care? Next we can tax Halloween & Valentines candy.

I suggest the legislators get their heads out of their ashtrays and work on:

Passing legislation to ensure all citizens have access to adequate medical care and affordable health insurance.

How about legislated affordable housing, free loans for everyone. While we are at it, I wonder if the legislature could do something about my neighbors alarm that seems to go off in the middle of the night whenever he is out of town.

I propose refusing to obey this law until our legislators demonstrate they really care about our health by passing measures that provide access to health care to all.

Actually Anthony, some states have already told carriers they must accept anyone who applies, regardless of their health history. States like MA, NY, ME, NH & VT have all prohibited carriers from excluding people regardless of health. In doing so, they have also just about tripled the cost of health insurance.

This guy is going to make a great lawyer.

Number Crunching...

Every once in a while, we run across interesting statidbits*:

For example, Ernst & Young surveyed Human Resources executives, asking which programs had the greatest impact on retaining older workers:

Turns out, almost 26% hired retirees as consultants. About 15% recommended a "company culture that promoted generational diversity" (don't ask), while another 15% used the oldest carrot in the book (in the form of retention bonuses). Interesting.

Here's another one:

According to the Employment Policies Institute, almost 90% of those employed full-time are covered by health insurance, as are over 80% of those working part-time. Almost the same percent of self-employed folks are also covered. and almost 2/3 of unemployed Americans also have health coverage.

Wow.

*Yes, I made that up. But "factoid" was already taken. I hate when that happens.

Tuesday, April 25, 2006

Gamblers

A growing number of small business owners and full-time workers make up about 80% of the America's 46 million people without health insurance.

According to this, only 20% of the uninsured population are unemployed or working part-time.

Nationwide, 16% of the population is uninsured, according to an October 2005 report from the Employee Benefits Research Institute.

Like those people, Wirthlin decided to risk it and forego health insurance coverage for him, his wife and their five children. Paying $180 for two doctor's office visits a year made much more sense to him than paying $400 to $500 a month in premiums.

You can see where this is going . . .

That logic worked until Wirthlin suffered a recent back injury. So far, he's paid $90 for an office visit and $600 for an MRI, which was about a 50% discount by the MRI provider when it learned Wirthlin was uninsured.

“The logic worked until . . .”

Too often people think health insurance is purchased to cover items you pay for on a regular basis. Yet this “logic” is not applied to other forms of insurance.

No one buys homeowners insurance to cover lawn maintenance or housecleaning. No one buys auto insurance to cover gasoline, tires & brakes. Why do we have people who think health insurance is bought to cover routine doctor visits?

The bills to date have been low because of a close friend who is an orthopedic surgeon, but if surgery is needed Wirthlin is looking at a bill in the tens of thousands of dollars. Right now he's waiting to see whether he'll have the surgery, which doctors have told him he needs.

Note to self. If you are going naked, make sure you have friends who are doctors that can treat you for free or at a discount.

"I wish I could have known that there would have been a catastrophic event so I could plan for it," Wirthlin said. "It's just one of those risks you take. In our case the risk didn't work out, but we were lucky for four years." “

I wish I could have known . . .”

Thing is, you can’t PLAN for a catastrophic event. What are you going to do? Set aside an extra $100,000 or so you have laying around the house for emergencies?

Even if you HAD $100,000 to spend on your catastrophic event, would it not be better to have paid $400 a month or so and let the carrier assume the risk?

According to this, only 20% of the uninsured population are unemployed or working part-time.

Nationwide, 16% of the population is uninsured, according to an October 2005 report from the Employee Benefits Research Institute.

Like those people, Wirthlin decided to risk it and forego health insurance coverage for him, his wife and their five children. Paying $180 for two doctor's office visits a year made much more sense to him than paying $400 to $500 a month in premiums.

You can see where this is going . . .

That logic worked until Wirthlin suffered a recent back injury. So far, he's paid $90 for an office visit and $600 for an MRI, which was about a 50% discount by the MRI provider when it learned Wirthlin was uninsured.

“The logic worked until . . .”

Too often people think health insurance is purchased to cover items you pay for on a regular basis. Yet this “logic” is not applied to other forms of insurance.

No one buys homeowners insurance to cover lawn maintenance or housecleaning. No one buys auto insurance to cover gasoline, tires & brakes. Why do we have people who think health insurance is bought to cover routine doctor visits?

The bills to date have been low because of a close friend who is an orthopedic surgeon, but if surgery is needed Wirthlin is looking at a bill in the tens of thousands of dollars. Right now he's waiting to see whether he'll have the surgery, which doctors have told him he needs.

Note to self. If you are going naked, make sure you have friends who are doctors that can treat you for free or at a discount.

"I wish I could have known that there would have been a catastrophic event so I could plan for it," Wirthlin said. "It's just one of those risks you take. In our case the risk didn't work out, but we were lucky for four years." “

I wish I could have known . . .”

Thing is, you can’t PLAN for a catastrophic event. What are you going to do? Set aside an extra $100,000 or so you have laying around the house for emergencies?

Even if you HAD $100,000 to spend on your catastrophic event, would it not be better to have paid $400 a month or so and let the carrier assume the risk?

Grand Rounds!

David Williams of the Health Business Blog, fresh off of hosting the Health Wonk Review earlier this month, has tackled this week's Grand Rounds. He managed to review, sort, and comment on 50 submissions. Outstanding!

As a beer connoisseur-wannabe, I loved this post from Dr Charles. Best of all, it has a VERY happy ending!

Monday, April 24, 2006

Short Doctors

After reading your recent article that discussed the shortage of doctors along the border, I have some thoughts I wish to express.

A large portion of the population in this area receives their medical coverage through Medicaid. Medicaid pays $29 for an average office visit. Most other insurances pay approximately $60 or more.

It should be noted that Medicare uses the same fee/reimbursement schedule as Medicaid. The issues raised in this article are not just limited to border towns, nor are they limited to Medicaid patients.

Also, other insurances [sic] will cover tests and services that the patient might need during their visit, whereas Medicaid does not allow for them or pays at a very discounted rate, to the point that one might actually lose money by providing the service.

How would you feel about being treated by a doctor that is losing money on your care?

Because of this, it takes at least two to three Medicaid patients to equal the revenue generated by one non-Medicaid insured patient.

By most medical personnel about the United States, a normal doctor load is approximately 30 patients per day.

In my practice, and I believe in many other practices in the area, 90 percent of the clientele is Medicaid. Therefore, in order to generate the income of a normal patient load elsewhere, we have to see double. In other words I have to see 60 patients to make the income of 30 patients.

Not only is the reimbursement to the doctor much lower, but the doctor must work twice as long to make the same money. This does not generate a warm feeling knowing I might be patient number 60 for the day.

As long as many doctors feel that to work in the border area they will have to see twice as many patients to generate an income equivalent to 30 patients elsewhere, the border will continue to have a doctor shortage.

A large portion of the population in this area receives their medical coverage through Medicaid. Medicaid pays $29 for an average office visit. Most other insurances pay approximately $60 or more.

It should be noted that Medicare uses the same fee/reimbursement schedule as Medicaid. The issues raised in this article are not just limited to border towns, nor are they limited to Medicaid patients.

Also, other insurances [sic] will cover tests and services that the patient might need during their visit, whereas Medicaid does not allow for them or pays at a very discounted rate, to the point that one might actually lose money by providing the service.

How would you feel about being treated by a doctor that is losing money on your care?

Because of this, it takes at least two to three Medicaid patients to equal the revenue generated by one non-Medicaid insured patient.

By most medical personnel about the United States, a normal doctor load is approximately 30 patients per day.

In my practice, and I believe in many other practices in the area, 90 percent of the clientele is Medicaid. Therefore, in order to generate the income of a normal patient load elsewhere, we have to see double. In other words I have to see 60 patients to make the income of 30 patients.

Not only is the reimbursement to the doctor much lower, but the doctor must work twice as long to make the same money. This does not generate a warm feeling knowing I might be patient number 60 for the day.

As long as many doctors feel that to work in the border area they will have to see twice as many patients to generate an income equivalent to 30 patients elsewhere, the border will continue to have a doctor shortage.

Monday Carnivals...

Despite some tech diff's (Blogger apparently suspended his "main" blog) , Clint at Million Dollar Goal is hosting this week's Carnival of Personal Finance.

He's chosen an interesting, if unorthodox, format: instead of listing each blog and its submission, he put posts into categories, sans blog or author. The idea is that, if you find a post's topic intriguing, you'll click thru to see where it is.

Which is what I did. We get a number of entrepreneurs here at IB; this post, at Frugal for Life, is the first in a two-part series on work-at-home scams, and how to avoid them.

And this week's Carnival of the Capitalists is up at the eponymously-named Entrepreneur's blog. Scott, our host, sifted through over 50 submissions, organizing and ranking them according to topic (and his review). Our own Bob Vineyard's post on High Deductible High Jinx was "Best in Category." WooHoo!

In keeping with the self-selected theme of entrepreneurship, take a moment to read Steve Pavlina's post on the 10 Stupid Mistakes Made by the Newly Self-Employed.

Charge it!

Growing up, “be careful what you wish for” was always a popular saying around my home. And, as a vocal (and vociferous) proponent of Consumer Driven Health Care, I should have seen this coming:

It seems that the convenience of these cards may also have a downside: as consumer credit card debts continues to climb (according to the article, it’s about $2,300 for the average citizen), charging health care could contribute to a substantial increase in such debt.

Now, I must confess that the concept of a “credit” card for HSA’s, FSA’s, and the like is somewhat foreign to me: I’ve always considered these to be more in the nature of debit cards. That is, they simply replace my checkbook when I’m paying for health care. Whatever funds are in the account represents the amount I have to spend; no more, no less.

So it came as a surprise to me (must be my sheltered existence) that financial service companies would set these up as unsecured lines of credit, as opposed to merely account balance conduits. But that’s apparently what is happening:

“The card, at a 12.96% interest rate, may be used to pay for elective or quality of life procedures, such as laser eye surgery, cosmetic dental care, orthodontry [sic] and hearing aids. Prices for such services easily go into the thousands, but Citi Health Card enables patients to "structure payment plans of up to 48 months, so members can customize their payments to fit their overall financial planning and medical spending."

The first two items, at least, aren’t even “kosher” by IRS standards; that is, they’re not eligible for tax free reimbursement under Section 213d. The beauty of our capitalist system is that folks are free (for the most part) to buy the things which are important to them.

Maybe I’m just a fuddy-duddy, but I’m skeptical that a credit card is the best vehicle for CDHP’s. Still, it will be interesting to see if the idea takes off.

Friday, April 21, 2006

Worst. Pre-Ex. Ever...

"An Oregon man who went to a hospital complaining of a headache was found to have 12 nails embedded in his skull from a suicide attempt with a nail gun, doctors say."

Oooookay.

But that's not the best part.

This is:

"The unidentified 33-year-old man was suicidal and high on methamphetamine last year when he fired the nails — up to 2 inches in length — into his head one by one."

Well, of course he shot them "one by one." Those semi-automatic nail guns are expensive!

On a sad note, the Darwin Awards have thus lost an outstanding nominee.

Oooookay.

But that's not the best part.

This is:

"The unidentified 33-year-old man was suicidal and high on methamphetamine last year when he fired the nails — up to 2 inches in length — into his head one by one."

Well, of course he shot them "one by one." Those semi-automatic nail guns are expensive!

On a sad note, the Darwin Awards have thus lost an outstanding nominee.

Stupid Carrier Tricks...

So Medical Mutual of Ohio (a fairly large, state-wide carrier) just bought Summit Insurance (a much smaller one). The deal’s been in the works for at least six months, and was finalized and announced a month or so ago.

So far, so good.

The actual transfer of business is set to take effect on May 1, so the carriers scheduled a series of meetings to familiarize brokers (agents) with what the sale means, what changes we can expect, and to answer any questions we might have.

Yesterday, I attended the last of 4 locally scheduled broker meetings:

First, the representative from Summit got up and spoke for about 45 minutes (which was approximately 35 minutes longer than was necessary). One could tell that the gentleman was not pleased to see his beloved company fade into oblivion, but we got that message pretty early on. He fielded a few questions, answering some, and passing others to the MMO person.

When Mr Summit was finished, he turned the meeting over to Ms MMO. She also spoke for a bit longer than was necessary.

There were, of course, a number of important (and urgent) items, but the two “take away” pieces were:

■ Although most maintenance prescriptions will (theoretically) transfer over from Summit to MMO, controlled substances and compounded meds will not; they will have to be re-prescribed. While this may not sound like a big deal, it certainly could be: physicians are restricted in how many of these scrips they can write for a given individual. Ooops.

■ Any procedures pre-authorized by Summit, which are scheduled for May 1 and later, must be re-authorized (by MMO). Granted, this makes sense from a claims standpoint, but announcing it only 10 days in advance is, well, stupid. How many such procedures will now have to be re-scheduled, as well?

The icing on this particular cake, however, took place near the end of the meeting. Our presenters had been unable to answer about half of our questions. So, I raised my hand:

“I have a more big picture question. Y’all have been working on this for over 6 months, and yet you’ve been unable to answer a lot of the questions we’ve asked today. And, this is the fourth such meeting you’ve held. We have no idea what questions were raised, and left unanswered, in the other three meetings. So, will there be an email or fax that addresses all these questions for us?”

Ms MMO replied that “that’d be a great idea. But we haven’t been writing them down, so we don’t know what all of them were.”

Yeah, me too.

A Study in Contrasts

The auto industry's efforts to rein in employee health costs is drawing an expensive reaction, as union workers and their spouses hurry to Michigan doctors for knee replacements and other elective procedures before they lose their comprehensive medical benefits.

Contrast this to another group whose benefits are provided under a single payor system.

The family of a 57-year-old Meath Park woman says it will take at least three months before their mother gets to see a Saskatchewan oncologist who can tell her if her cancer is treatable or fatal.

One group has virtually free and unlimited access to health care.

Hip, knee and shoulder replacements at the Henry Ford Health System were "up 20 percent in the second half of last year and remain strong," said Robert Riney, chief operating officer of the system, the largest hospital group in the Detroit area.

The other has free but LIMITED access to health care.

Emily Morley has already waited a month to see an oncologist since receiving her biopsy results that identified her secondary cancer, but were inconclusive in determining the primary source. Until that primary source is identified, her treatment cannot begin.

And even though the cancer is now in Morley's lungs, liver, pancreas and spine, the Saskatoon Cancer Clinic has advised her it will still take at least three months to see an oncologist.

One group is almost pillaging the coffers for elective procedures that will improve the quality of life but not extend it.

"In the last six months, we've noticed a significant increase in people seeking elective surgical procedures in anticipation that they might be losing their health benefits," Mr. Riney said. He would not say how much his health system was billing the auto industry because of the last-minute rush to have elective procedures performed.

While the other is simply hoping to stay alive.

"As of this point, she doesn't even know if this is terminal or not," her son Chris Andersen told reporters at the legislature Wednesday.

And folks say OUR health care system is broken.

Contrast this to another group whose benefits are provided under a single payor system.

The family of a 57-year-old Meath Park woman says it will take at least three months before their mother gets to see a Saskatchewan oncologist who can tell her if her cancer is treatable or fatal.

One group has virtually free and unlimited access to health care.

Hip, knee and shoulder replacements at the Henry Ford Health System were "up 20 percent in the second half of last year and remain strong," said Robert Riney, chief operating officer of the system, the largest hospital group in the Detroit area.

The other has free but LIMITED access to health care.

Emily Morley has already waited a month to see an oncologist since receiving her biopsy results that identified her secondary cancer, but were inconclusive in determining the primary source. Until that primary source is identified, her treatment cannot begin.

And even though the cancer is now in Morley's lungs, liver, pancreas and spine, the Saskatoon Cancer Clinic has advised her it will still take at least three months to see an oncologist.

One group is almost pillaging the coffers for elective procedures that will improve the quality of life but not extend it.

"In the last six months, we've noticed a significant increase in people seeking elective surgical procedures in anticipation that they might be losing their health benefits," Mr. Riney said. He would not say how much his health system was billing the auto industry because of the last-minute rush to have elective procedures performed.

While the other is simply hoping to stay alive.

"As of this point, she doesn't even know if this is terminal or not," her son Chris Andersen told reporters at the legislature Wednesday.

And folks say OUR health care system is broken.

Thursday, April 20, 2006

Health Wonk Review, WooHoo!

The fifth installment of HWR is up at the Envisioning blog. This bi-weekly compendium continues to grow, and this week's version is particularly well put-together. Make sure to check out each of the Einstein "photo's."

Since Consumer Driven Health Care is a something of a meme here at IB, I particularly appreciated FoIB MarketPlace, MD's announcement of a "Blogposium" on CDHC. An extremely informative and interesting piece.

Wednesday, April 19, 2006

Norris vs Annuities: A Reality Check

No, not that Norris: One of our clients is a law firm which deals with administrative and compliance issues for qualified plans. For example, they’re the folks that take care of our agency’s 401(k). We’ve always had a good relationship with the firm, and it recently got even better:

Turns out that one of their other clients is a reasonably large local financial services firm, from which a number of folks will be retiring over the next few months and years. They have a “defined contribution” plan, which guarantees a lump sum to each participant, and from which each participant will receive a monthly income. The vehicle of choice for such applications is a Single Premium Immediate Annuity.

SPIA’s are custom made for this. I give the computer (or the carrier) the participant’s age, sex and the lump sum amount, and I get the monthly income that each participant will receive for as long as they live. Simple enough, right?

Not so fast, Buckaroo:

Back in 1983, the Supreme Court handed down what’s come to be known as the Norris Decision. Because women (as a group) outlive men (as a group), the monthly benefit amount which a woman would receive from a given lump sum is less than the amount for the man. Makes sense: the original sum has to last longer, in general.

Norris, though, said that such discrimination violated the ban against sex discrimination in employment in Title VII of the '64 Civil Rights Act. So, an annuity which used gender-specific assumptions was a no-no. The upshot is that in cases which must be Norris-compliant, one needs to use a unisex annuity. Simple enough.

Except that there is no such animal. By definition, annuities which pay a lifetime income are based on the sex of the annuitant. But that doesn’t matter to Norris, which bans such discrimination even if the only annuities available are based on sex-segregated annuity tables.

Ooops.

So now what?

Well, it turns out that there is a plan available that seems to meet the Norris challenge. It was, in fact, designed specifically to do so. The only drawback, if there is one, is that it is a group annuity, which the employer (plan) itself owns. And it is this program which I’ll be looking to as I continue working on this case. My only real problem with this is that I like to have choices for my clients, and this seems to be the only such product on the market.

Still, beats having to say “sorry, I can’t help you.”

Babe Alert!

Jenni, hostess of ChronicBabe, has kindly linked us as one of her Fab Five favorite sites. She says InsureBlog is a "smart (that would be me) and snarky (that you, Bob?) look at all things insurance."

Thanks for the kudos, and back at ya!

Tuesday, April 18, 2006

Retro Underwriting

This has nothing to do with underwriters wearing Madras shirts with pocket protectors. Retrospective underwriting, or retro underwriting, is the practice utilized by some health insurance carriers to cancel coverage and rescind back to the effective date.

This usually occurs following a claim of some significance when an audit of the underwriting file is ordered. Consider this a post-mortem on an underwriting decision made as far back as 2 year ago.

The scenario could go something like this.

You complete an application for health insurance and submit it to a carrier, we will call them Indigo Cross Health Insurance Company. In the litany of questions is one of note.

Have you ever been diagnosed, treated for or consulted with a medical professional for any of the following:

Blah, blah, blah, cancer, blah, blah.

Have you ever experienced any of the following:

Unexplained fever, swollen glands, abdominal, back or pelvic pain, . . . .

Your answer to all of the questions is “no”

The policy is issued.

Three months later you go to the doctor complaining of a pain in your gut that won’t go away.

How long have these symptoms persisted?

Off and on, maybe 4 or 5 months, but they are more painful now.

Tests are performed and the diagnosis comes back. You have colon cancer.

Then you get a letter from your carrier, denying your claim and rescinding coverage back to the effective date.

You have just entered the world of retro underwriting. In addition to dealing with the diagnosis, you now have to wonder how you will pay for your care.

Like it or not, the carrier has not only denied your claim, but cancelled coverage based on what is considered to be a false application. You misrepresented the facts by failing to mention an undiagnosed pain.

This was coupled with the admission, as reflected in the doctors notes, that this pain existed prior to the date of your application.

Is this practice fair? Yes, and no. It can be argued both ways.

Is this something to consider the next time you submit an application for insurance?

Absolutely.

This usually occurs following a claim of some significance when an audit of the underwriting file is ordered. Consider this a post-mortem on an underwriting decision made as far back as 2 year ago.

The scenario could go something like this.

You complete an application for health insurance and submit it to a carrier, we will call them Indigo Cross Health Insurance Company. In the litany of questions is one of note.

Have you ever been diagnosed, treated for or consulted with a medical professional for any of the following:

Blah, blah, blah, cancer, blah, blah.

Have you ever experienced any of the following:

Unexplained fever, swollen glands, abdominal, back or pelvic pain, . . . .

Your answer to all of the questions is “no”

The policy is issued.

Three months later you go to the doctor complaining of a pain in your gut that won’t go away.

How long have these symptoms persisted?

Off and on, maybe 4 or 5 months, but they are more painful now.

Tests are performed and the diagnosis comes back. You have colon cancer.

Then you get a letter from your carrier, denying your claim and rescinding coverage back to the effective date.

You have just entered the world of retro underwriting. In addition to dealing with the diagnosis, you now have to wonder how you will pay for your care.

Like it or not, the carrier has not only denied your claim, but cancelled coverage based on what is considered to be a false application. You misrepresented the facts by failing to mention an undiagnosed pain.

This was coupled with the admission, as reflected in the doctors notes, that this pain existed prior to the date of your application.

Is this practice fair? Yes, and no. It can be argued both ways.

Is this something to consider the next time you submit an application for insurance?

Absolutely.

Department of Counterintuition…

And yes, I (think) I just made up a new word. But it seems to fit; according to a new study in the New England Journal of Medicine:

The study purports to show that excising limits on services for mental health and substance abuse does not drive up health insurance costs, and eliminating caps (e.g. on the number of therapy sessions or days in a psych ward) does not boost spending. The "gotcha," though, is interesting: in this study, parity went hand-in-hand with managed care, which has had something of a cool reception from the behavioral health community.

The study compared several federal (government) plans that offered mental health and substance-abuse services equal to general medical benefits to plans that did not offer such cover. Of the seven, only one showed a considerable increase in usage of services, while another showed a marked decrease in usage; the rest showed little change. “Plan costs decreased in three plans and did not change in the other four. Out-of-pocket spending on mental health services decreased in five of the seven plans, according to the research.”

While I’m skeptical that adding more covered benefits doesn’t increase utilization, and costs, this study does make a certain sense: after all, the insurance industry has been touting the case for managed care for a long time, so it seems consistent that mental health cover could benefit from a little, as well.

Puts my mind at ease.

'Tis Time for Grand Rounds

And a fine job Fat Doctor does, at that. Over 50 entries, all arranged into "broad categories," including BODY PARTS AND BROKEN HEARTS. Oy!

I was most intrigued by Dr Bob's post explaining the medical coding process, and highlighting some of its history.

Monday, April 17, 2006

The (expensive) Little Blue Pill

For many years, armchair pundits have claimed that men’s fascination with the automobile is symbolic. Well, it turns out that this wasn’t so far off the mark:

In fairness, this was a concession hard-won by the workers’ union, which dictated that such lifestyle drugs be covered by their members’ insurance:

"Once you have these benefits, it's very difficult to take them away," said Jim Sanfilippo, president of AMC Inc., an industry consultancy in Detroit."

And, of course, an aging workforce also contributes to the demand:

“(G)iven the huge number of older GM workers who might need help to "keep the spark alive," the tab for Viagra and other erectile dysfunction drugs isn't likely to go down soon.”

This challenge mirrors current health care insurance issues in general: how to keep costs in line while maintaining needed (or just desired) coverage. Whether we’re talking about Viagra, IVF, or birth control, lifestyle medications do impact the overall cost of health insurance, and seem like a reasonable place to start when we talk about medically unnecessary treatments.

Proton Pump Inhibitors

“Scottie, I need more power to the Proton Pump Inhibitors”! Proton Pump Inhibitors (PPI) may sound like something from a Star Trek movie, but it isn’t.

Instead, a PPI is a medicine to treat heartburn.

Aetna (NYSE: ΑET) is launching a six-month pilot program in the New Jersey area that waives copays for fully insured members changing to generic from brand name proton pump inhibitors (PPI) to treat heartburn or similar symptoms.

Commercial plan members currently filling prescriptions for certain brand name PPIs are eligible for the copay waiver, if they switch therapy to the generic omeprazole 20mg (the generic for Prilosec®).

Pricing 30 tabs at a major chain indicates 20mg Prilosec will run about $160.

Compare that to $15 for generic at Pharmacymex.

It is unclear from the news item if Omeprazole is available in the U.S. or if the plan will allow across the border imports. Many health insurance plans do not cover mail order meds from outside the U.S.

So how much can Aetna save if this change is successful?

Aetna estimates that more than 19,000 of its members in the New Jersey area are now receiving PPI medications, at an annual cost of $3 million

That is a significant number that cannot be ignored.

Here is another interesting tidbit to throw out at cocktail parties.

According to the Generic Pharmaceutical Association, half the prescriptions being filled in the U.S. are for generics, but annual expenditures for those medications only represent between 10 and 15 percent of the cost for prescriptions in the U.S.

Beam me up Scottie.

Instead, a PPI is a medicine to treat heartburn.

Aetna (NYSE: ΑET) is launching a six-month pilot program in the New Jersey area that waives copays for fully insured members changing to generic from brand name proton pump inhibitors (PPI) to treat heartburn or similar symptoms.

Commercial plan members currently filling prescriptions for certain brand name PPIs are eligible for the copay waiver, if they switch therapy to the generic omeprazole 20mg (the generic for Prilosec®).

Pricing 30 tabs at a major chain indicates 20mg Prilosec will run about $160.

Compare that to $15 for generic at Pharmacymex.

It is unclear from the news item if Omeprazole is available in the U.S. or if the plan will allow across the border imports. Many health insurance plans do not cover mail order meds from outside the U.S.

So how much can Aetna save if this change is successful?

Aetna estimates that more than 19,000 of its members in the New Jersey area are now receiving PPI medications, at an annual cost of $3 million

That is a significant number that cannot be ignored.

Here is another interesting tidbit to throw out at cocktail parties.

According to the Generic Pharmaceutical Association, half the prescriptions being filled in the U.S. are for generics, but annual expenditures for those medications only represent between 10 and 15 percent of the cost for prescriptions in the U.S.

Beam me up Scottie.

Money Monday: Carnivals

This week's edition of the Carnival of Personal Finance is already up at Five Cent Nickel. With 34 entries(!), you're sure to find something interesting, or at least though-provoking. I know I did: this entry from Matt Inglot explains that money is really just a tool, and why that's important to understand.

Not far behind, the Free Money Finance hosts this week's Carnival of the Capitalists. This edition boasts 43 entries, all arranged in helpful, useful categories. For a bit of whimsy, check out this post explaining the economics of Harry Potter's world.

Friday, April 14, 2006

Color Me Skeptical...

In the world according to AARP, about half the folks on Medicare lacked coverage for prescription meds; Part D has apparently helped reduce those numbers. The upside is that the new plan has helped those who’ve opted in to save some significant dollars on prescriptions.

On the other hand, "(m)illions of senior citizens have not signed up for and do not know much about" it. Almost 30 million of our seasoned citizens have signed up for Part D, but between 8 and 14 million are playing “wait and see.” Which is, of course, their right to do, even as the clock winds down on the May 15 deadline.

Not surprisingly, “(t)he drug benefit is being accepted more warmly by those who stand to take personal advantage of it than by the public at large. Half of the seniors polled approve of the plan, compared with 41 percent who disapprove.” That seems to me to be just common sense: of course those who directly benefit from a given program are going to be more favorably disposed towards it than those who are actually paying the freight.

One line in the Yahoo article jumped out at me:

“AARP is working to make the Medicare drug program even stronger by allowing HHS to negotiate drug prices for the program.”

Now, perhaps I’m reading this wrong, but I was not aware that AARP had such an unprecedented influence on the Executive Branch; I sure hope W had the courtesy of sending them a Thank You note.

Even more interesting is that, according to FoIB Kate Steadman, AARP “once supported the pharmaceutical companies' inalienable rights to demand their highest prices, AARP is now calling for the government to negotiate.”

Even stranger, she reveals that, just a few years ago, the organization “went so far as to sponsor their own Medicare Part D Plan.” And that their own studies showed that “prices in the new prescription drug benefit were lower than buying drugs from Canada.”

So which is it?

NY NY

Start spreading the news

I'm leaving today

Frank Sinatra “owned” that song. As the song progresses you find someone who wants to be in New York, the city that never sleeps.

But the Fair Share Health Care Act could drive people away from New York if fully implemented.

The act is like the Maryland proclamation on steroids.

New York’s so-called “Fair Share for Health Care Act” imposes a pay-or-play health insurance mandate on firms with 100 or more employees. These firms employ more than 70 percent of New York’s workforce, and would be subject to a tax as high as $3 per hour for covered workers. As a consequence, a firm employing a full-time, full-year worker could be subject to an additional annual labor cost of as much as $6,000.

Ouch!

Beats the heck out of the neighboring Massachusetts penalty of $295 per year.

A firm could react to the mandate by adjusting hiring practices, relocating out of New York, raising output prices, reducing the quality of their product, accepting lower profitability, or going out of business. Previous economic work suggests wage shifting is a likely response. When such an offset is not possible (due to New York’s minimum wage of $6.75 per hour), the mandate is likely to destroy jobs.

It get’s worse . . .

For those close to the minimum wage, wage shifting is not possible and employment losses ensue. The estimates suggest that between 37,000 and 65,000 low-wage workers will lose their jobs

Don’t you just love it when politicians mess with a system and make it worse?

I'm leaving today

Frank Sinatra “owned” that song. As the song progresses you find someone who wants to be in New York, the city that never sleeps.

But the Fair Share Health Care Act could drive people away from New York if fully implemented.

The act is like the Maryland proclamation on steroids.

New York’s so-called “Fair Share for Health Care Act” imposes a pay-or-play health insurance mandate on firms with 100 or more employees. These firms employ more than 70 percent of New York’s workforce, and would be subject to a tax as high as $3 per hour for covered workers. As a consequence, a firm employing a full-time, full-year worker could be subject to an additional annual labor cost of as much as $6,000.

Ouch!

Beats the heck out of the neighboring Massachusetts penalty of $295 per year.

A firm could react to the mandate by adjusting hiring practices, relocating out of New York, raising output prices, reducing the quality of their product, accepting lower profitability, or going out of business. Previous economic work suggests wage shifting is a likely response. When such an offset is not possible (due to New York’s minimum wage of $6.75 per hour), the mandate is likely to destroy jobs.

It get’s worse . . .

For those close to the minimum wage, wage shifting is not possible and employment losses ensue. The estimates suggest that between 37,000 and 65,000 low-wage workers will lose their jobs

Don’t you just love it when politicians mess with a system and make it worse?

Pay Before Pumping

As gas prices continue to rise many of the self serve gas stations (are there any full service stations left?) have instituted a policy of paying before you pump. Makes sense. If you pull into a station with your SUV running on fumes you could easily pump $50 or more into the tank before it tops off. To avoid drive-offs, scofflaws who feel they are entitled to take a 5 finger discount on gas, you now have to pay before the pump is activated.

Seems many docs are doing the same.

Collecting balances due has always been a problem for physicians

So why not do what a growing number of businesses, including every hotel, motel, and country inn on the planet, already do: Ask each patient for a credit card, take an imprint, and bill balances to it as they accrue.

Makes sense to me.

Seems many docs are doing the same.

Collecting balances due has always been a problem for physicians

So why not do what a growing number of businesses, including every hotel, motel, and country inn on the planet, already do: Ask each patient for a credit card, take an imprint, and bill balances to it as they accrue.

Makes sense to me.

Thursday, April 13, 2006

TV Causes . . .

Watching TV could be hazardous to your health, and wallet.

Until a few years ago I never knew women had vaginal itch and men had erectile dysfunction. I always assumed my toenails were just supposed to have a yellow tint and certainly did not know there could be yellow demons living under the nail that caused the discoloration.

Only recently did I learn that high cholesterol is not caused by eating double cheeseburgers for lunch but that I could blame my Aunt Jenny or Uncle Ed for this “illness”. Neither did I know that chest congestion was caused by a critter living in my lungs, complete with a couch & all the comforts of home.

In this fast paced society it seems no one has time to actually correct an illness or affliction. Instead, just pop a pill.

At one time shows like Mary Hartman & Soap were considered risqué.

Now it’s the advertisements that are discussing things that were once only talked about at a ladies bridge party.

Commercials can inform and can even entertain. Who would have known headaches were caused by a hammer against an anvil inside your head if it weren’t for the Anacin commercials years ago?

But commercials can also lead one to believe a common occurrence is something that requires a $200 drug in order to provide relief.

Sure I get edgy sometimes, but it really isn’t my fault. I know what causes the problem.

I learned that years ago.

From TV.

Everything can be blamed on mom.

“Mother please! I’d rather do it myself”!

Until a few years ago I never knew women had vaginal itch and men had erectile dysfunction. I always assumed my toenails were just supposed to have a yellow tint and certainly did not know there could be yellow demons living under the nail that caused the discoloration.

Only recently did I learn that high cholesterol is not caused by eating double cheeseburgers for lunch but that I could blame my Aunt Jenny or Uncle Ed for this “illness”. Neither did I know that chest congestion was caused by a critter living in my lungs, complete with a couch & all the comforts of home.

In this fast paced society it seems no one has time to actually correct an illness or affliction. Instead, just pop a pill.

At one time shows like Mary Hartman & Soap were considered risqué.

Now it’s the advertisements that are discussing things that were once only talked about at a ladies bridge party.

Commercials can inform and can even entertain. Who would have known headaches were caused by a hammer against an anvil inside your head if it weren’t for the Anacin commercials years ago?

But commercials can also lead one to believe a common occurrence is something that requires a $200 drug in order to provide relief.

Sure I get edgy sometimes, but it really isn’t my fault. I know what causes the problem.

I learned that years ago.

From TV.

Everything can be blamed on mom.

“Mother please! I’d rather do it myself”!

Wednesday, April 12, 2006

Dale Carnegie: Spinning...

This will probably be a fairly long rant, so please be patient with me.

The title of this post refers to the great motivational author and speaker, Dale Carnegie, and his classic tome "How to Win Friends and Influence People." In it, he teaches folks effective means of communication, both in business and personal relationships.

The experience I'm about to relate might be titled "How to Effectively Damage Your Business, and Squander Years of Good Will."

Although ours is an independent agency, my P&C colleagues place the bulk of their business with a specific carrier. This is neither good nor bad, it just is. For a number of reasons, I have given this carrier's life insurance subsidiary "first dibs" on the life business that I write.

Each spring, this carrier puts on a sort of traveling roadshow, called the Annual Sales Meeting. Folks from the home office travel all over the midwest, and it gives both the agents and the home office staff the opportunity to mingle, and to share experiences and ideas. It's a lot of fun, and I look forward to them.

This year's would have been my 22nd consecutive meeting.

You'll notice I said "would have been." That's because the meeting was scheduled for the first night of Passover. This is a significant and special Holy Day, and is marked on most calendars. Now, I don't think that anyone intentionally set out to offend those of us in the field who are Jewish; most likely, it just never occurred to whomever set the dates to even check.

I was, at first, annoyed at this oversight; the more I thought about, the more irritated I became. Knowing my own limitations, I knew that I needed to tell someone how I felt, so I called the home office, and asked for the office of the CEO (hey, it's not like I have any problem calling the head honcho). I didn't really expect to speak with him personally; I just wanted to make sure that he knew that I was disappointed to miss the meeting, and offended at the reason that this was so.

My colleagues were split as to whether they thought I'd get an apologetic return call or not. I predicted that I wouldn't hear anything about it.

I was wrong.

This morning, I received a call from the Regional Sales Manager for the carrier, chastising me for not "going through channels." No acknowledgement of the offense, just a "slap on the wrist" about following their protocol.

Regular readers (and those who know me personally) will be pleased, if not shocked, to learn that I did not, in fact, lose my temper. I politely, but firmly, told the gentleman that, first, I did not want to say or do anything to damage the relationship between our agency and his company. But, I explained, I did not care about his protocol, because I do not work for him or his company. He was momentarily taken aback, but pressed on, admitting that he didn't see what I was so offended about in the first place.

At that point, I told him that, contrary to his intent, he was not helping his own cause. Indeed, he was offending me even more. I explained that I was anticipating an apology (at best), and that I would have also accepted no response at all. I concluded by asking him if there was anything else I could do for him, and we concluded our conversation.

In addition to representing this carrier, I have been a customer for over 20 years, as well: my home, auto, umbrella and much of my life insurance has been with them. As soon as we hung up, I buzzed one of my colleagues and asked her to get me the numbers for moving all of my P&C cover to our other primary company. I have also determined that I no longer feel comfortable placing business with this carrier: I am currently working on 6 life cases, all of which I will now place with other carriers.

What's so disappointing about this is that the gentleman has irreconcilably destroyed over 20 years of good-will and customer satisfaction. I sure hope he's happy.

ADDENDUM: In reviewing the phone conversation, I recalled another telling piece of information. At the very beginning of the call, the gentleman mentioned that he had received an email directing him to call me. Since I had spoken only with the CEO's office, I can only conclude that this gentleman's opinions represent those of the company itself; that is, the CEO had obviously directed him to inform me of my faux pas, and to abstain from any apology. That also speaks volumes.

The title of this post refers to the great motivational author and speaker, Dale Carnegie, and his classic tome "How to Win Friends and Influence People." In it, he teaches folks effective means of communication, both in business and personal relationships.

The experience I'm about to relate might be titled "How to Effectively Damage Your Business, and Squander Years of Good Will."

Although ours is an independent agency, my P&C colleagues place the bulk of their business with a specific carrier. This is neither good nor bad, it just is. For a number of reasons, I have given this carrier's life insurance subsidiary "first dibs" on the life business that I write.

Each spring, this carrier puts on a sort of traveling roadshow, called the Annual Sales Meeting. Folks from the home office travel all over the midwest, and it gives both the agents and the home office staff the opportunity to mingle, and to share experiences and ideas. It's a lot of fun, and I look forward to them.

This year's would have been my 22nd consecutive meeting.

You'll notice I said "would have been." That's because the meeting was scheduled for the first night of Passover. This is a significant and special Holy Day, and is marked on most calendars. Now, I don't think that anyone intentionally set out to offend those of us in the field who are Jewish; most likely, it just never occurred to whomever set the dates to even check.

I was, at first, annoyed at this oversight; the more I thought about, the more irritated I became. Knowing my own limitations, I knew that I needed to tell someone how I felt, so I called the home office, and asked for the office of the CEO (hey, it's not like I have any problem calling the head honcho). I didn't really expect to speak with him personally; I just wanted to make sure that he knew that I was disappointed to miss the meeting, and offended at the reason that this was so.

My colleagues were split as to whether they thought I'd get an apologetic return call or not. I predicted that I wouldn't hear anything about it.

I was wrong.

This morning, I received a call from the Regional Sales Manager for the carrier, chastising me for not "going through channels." No acknowledgement of the offense, just a "slap on the wrist" about following their protocol.

Regular readers (and those who know me personally) will be pleased, if not shocked, to learn that I did not, in fact, lose my temper. I politely, but firmly, told the gentleman that, first, I did not want to say or do anything to damage the relationship between our agency and his company. But, I explained, I did not care about his protocol, because I do not work for him or his company. He was momentarily taken aback, but pressed on, admitting that he didn't see what I was so offended about in the first place.