Friday, April 28, 2017

Thursday, April 27, 2017

MVNHS© Strikes Again

As we've noted countless times, government-run healthcare means rationed healthcare. There just isn't any other way to manage costs (for certain values of "manage"). This time out, the Much Vaunted National Health System© has its sights set on those who smoke and/or need to shed a few stone:

"NHS bosses are planning a massive expansion of the controversial rationing that forces smokers and obese patients to wait months in pain before they can have surgery"

Keep in mind, this is in addition to the already scandalous wait times facing lean non-smokers.

On its face, this seems reasonable enough: after all, this is primarily about lifestyle choices one has made (to smoke or overindulge at the buffet). But here's the thing: these folks still pay the same in taxes as their non-smoking, skinny fellow Britons, yet are going to be denied timely medical care. But if the point of the exercise is "fairness" (as it seems to be), well: #Fail.

[Hat Tip: MisHum]

"NHS bosses are planning a massive expansion of the controversial rationing that forces smokers and obese patients to wait months in pain before they can have surgery"

Keep in mind, this is in addition to the already scandalous wait times facing lean non-smokers.

On its face, this seems reasonable enough: after all, this is primarily about lifestyle choices one has made (to smoke or overindulge at the buffet). But here's the thing: these folks still pay the same in taxes as their non-smoking, skinny fellow Britons, yet are going to be denied timely medical care. But if the point of the exercise is "fairness" (as it seems to be), well: #Fail.

[Hat Tip: MisHum]

Wednesday, April 26, 2017

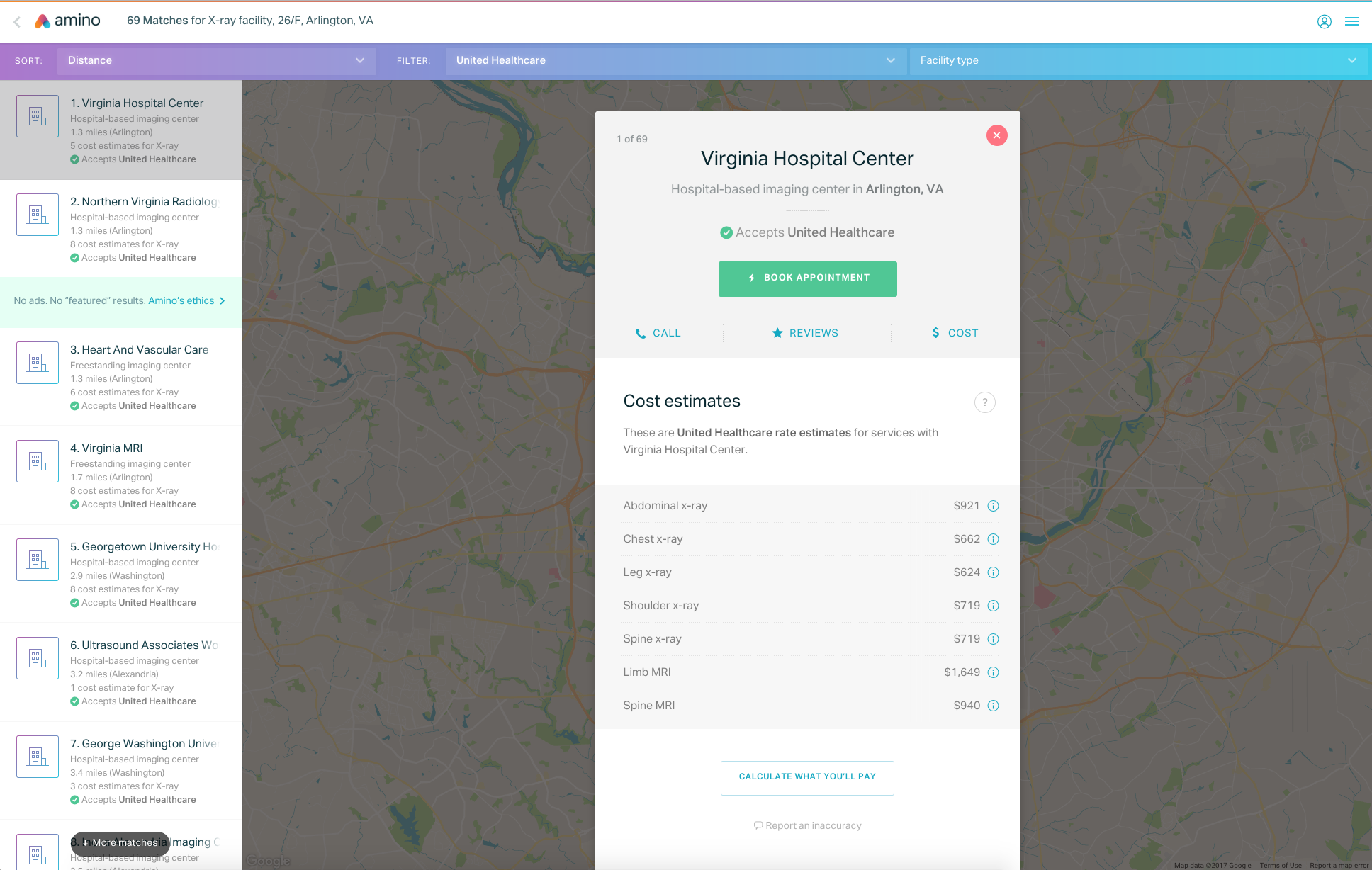

Zillow for Healthcare

Earlier this month, I posted on how a SoCal clinic had (finally) provided an example of my personal healthcare Holy Grail, a truly transparent healthcare pricing model. The challenge is that it's specific to this small, regional chain of clinics,and doesn't really help folks outside the immediate area, or with comparison to other providers (which don't share this information).

Now comes Amino, which "gives patients access to information on the cost of various procedures and how much experience doctors nationwide have in those procedures."

And there's no charge for using it.

The site is the brainchild of a former Zillow alum who was frustrated in his own efforts to find this kind of information for his own health issues:

"I realized just having the consumer experience that health care had offered me was really frustrating ... So I decided to build Amino to solve that.”

Now comes Amino, which "gives patients access to information on the cost of various procedures and how much experience doctors nationwide have in those procedures."

And there's no charge for using it.

The site is the brainchild of a former Zillow alum who was frustrated in his own efforts to find this kind of information for his own health issues:

"I realized just having the consumer experience that health care had offered me was really frustrating ... So I decided to build Amino to solve that.”

Of course, this really isn't critical if one has no skin in the game, so it will be most valuable for folks with (for example) HSA-type plans:

“When people pay their own way, they’ll start to shop and demand prices [says Twila Brase, president of the consumer group Citizens’ Council for Health Freedom] ... Lots of people wanted to force doctors to be transparent about their prices, but it didn’t matter until people pay their bills.”

Yup. Now, if we could just get to truly catastrophic coverage, these types of services should really take off.

[Hat Tip: The Political Hat]

“When people pay their own way, they’ll start to shop and demand prices [says Twila Brase, president of the consumer group Citizens’ Council for Health Freedom] ... Lots of people wanted to force doctors to be transparent about their prices, but it didn’t matter until people pay their bills.”

Yup. Now, if we could just get to truly catastrophic coverage, these types of services should really take off.

[Hat Tip: The Political Hat]

Tuesday, April 25, 2017

Passive vs Active Mortality

A couple of months ago, we blogged on the fact that, among other failures, ObamaCare hasn't actually saved any lives, and that "public health trends since the implementation of the ACA have worsened."

Bad as that may be (and it is awful), it pretty much describes a status quo as regards pre-O'Care healthcare financing (insurance) and delivery.

But what if it's actually worse than this?

Well, thanks to FoIB Holly R, we learn that it is:

"Mortality Rates Suggests Obamacare Could Be Killing People ... equivalent to an excess 11,000 annual U.S. adult deaths relative to the pre-Obamacare steady state trends"

This despite correcting for the increasing death toll from the opioid crisis (and similar factors). In other words, ObamaCare has a body count:

Bad as that may be (and it is awful), it pretty much describes a status quo as regards pre-O'Care healthcare financing (insurance) and delivery.

But what if it's actually worse than this?

Well, thanks to FoIB Holly R, we learn that it is:

"Mortality Rates Suggests Obamacare Could Be Killing People ... equivalent to an excess 11,000 annual U.S. adult deaths relative to the pre-Obamacare steady state trends"

This despite correcting for the increasing death toll from the opioid crisis (and similar factors). In other words, ObamaCare has a body count:

Now, it's fair to say that we don't know which part of The ObamaTax is responsible for this spike, but I would argue that this is just another reason for its full repeal, not DC rocket surgeon tweaking; the stakes are just too high.

But maybe that's just me.

But maybe that's just me.

Feds make argument against single payer

For all the hoopla over the benefits of government-run health care schemes, one would think that the Feds would be all-in on the concept. And yet, much as Britain's MVNHS© has spawned private plans, the US government seems to be throwing at least one single-payer, government-run healthcare system under the bus:

"President Trump signed a very important bill on Wednesday that extended the Veterans Choice Program ... The bill will allow veterans to seek private care outside of the VA"

Now, there are some conditions attached: the vet must live at least 40 miles away from the nearest VA hospital, or be unable to book an appointment within a30 days. On the other hand, it's at least an acknowledgement that there aren't enough facilities, and that those that doe exist are frequently overbooked and/or understaffed.

So, at least some choice is now available to those who risked their lives in service to their country. And further proof - as if that's necessary - that single payer, government-run health care is, at best, sub-standard.

"President Trump signed a very important bill on Wednesday that extended the Veterans Choice Program ... The bill will allow veterans to seek private care outside of the VA"

Now, there are some conditions attached: the vet must live at least 40 miles away from the nearest VA hospital, or be unable to book an appointment within a30 days. On the other hand, it's at least an acknowledgement that there aren't enough facilities, and that those that doe exist are frequently overbooked and/or understaffed.

So, at least some choice is now available to those who risked their lives in service to their country. And further proof - as if that's necessary - that single payer, government-run health care is, at best, sub-standard.

Monday, April 24, 2017

Buddy, Can You Spare a Dime?

Medical bills piling up? No problem. Just stiff the health care provider. Why not. You got the treatment. You feel better. Doctors and hospitals make a lot of money. They can afford to write off my bill.

Sadly, far too many people have that attitude.

Obamacare didn't CAUSE this problem, but the number of patients willing to skate on paying a medical bill is on the rise. Higher premiums. Higher deductibles. Higher out of pocket.

Even if the patient WANTS to pay their bill, often they can't. A Kaiser study confirms this.

Four in ten (43 percent) adults with health insurance say they have difficulty affording their deductible, and roughly a third say they have trouble affording their premiums and other cost sharing; all shares have increased since 2015.

Three in ten (29 percent) Americans report problems paying medical bills, and these problems come with real consequences for some. For example, among those reporting problems paying medical bills, seven in ten (73 percent) report cutting back spending on food, clothing, or basic household items.

Challenges affording care also result in some Americans saying they have delayed or skipped care due to costs in the past year, including 27 percent who say they have put off or postponed getting health care they needed, 23 percent who say they have skipped a recommended medical test or treatment, and 21 percent who say they have not filled a prescription for a medicine.

Even for those who may not have had difficulty affording care or paying medical bills, there is still a widespread worry about being able to afford needed health care services, with half of the public expressing worry about this.

Almost half of people would have difficulty paying a $500 medical bill. About one in five would not be able to pay that bill at all.

While some see this as an indictment of the current health care and health insurance system, it is also a statement about money management skills.

#MedicalDebts #UnaffordableHealthCare #Obamacare #Medicare

Ominous sign

We last seriously discussed worksite life plans back in 2011:

"The basic idea, though, remains the same: small face amounts, simplified underwriting and easily-budgeted premiums"

At the time, we noted that the market was facing a rather serious challenge:

"U.S. sales of voluntary group insurance products and individual products sold at the worksite fell 2.9% in 2010."

Now, that original post didn't differentiate between life and other insurance products available through these kinds of arrangements, but at least some of these numbers reflect life insurance sales.

Now there's even more bad news, and this is specifically related to payroll deduction (worksite marketed) life insurance:

"Middle-aged white Americans without four-year degrees are at increasing risk of dying [prematurely]."

There are, of course, any number of possible explanations for this, but Bloomberg's Jeanna Smialek puts the blame on drug and alcohol abuse, and "slowing progress against heart disease and cancer."

I'm not quite in agreement on this: after all, black men (and white women) face the same challenges, and I don't see evidence cited that they're dying any earlier. And this is drivel:

"For all the debate over whether college is worthwhile, high school graduates who go straight into the workforce have higher unemployment [and] weaker wage growth" than their college-educated peers.

Really?

They also have zero college debt, and at least least 4 years of wage-earning over their college-educated peers. And if they're in the trades, the odds are pretty good that they're going to earn more - perhaps a lot more - than the barrista with the 6 year feminist studies degree.

Something to consider.

"The basic idea, though, remains the same: small face amounts, simplified underwriting and easily-budgeted premiums"

At the time, we noted that the market was facing a rather serious challenge:

"U.S. sales of voluntary group insurance products and individual products sold at the worksite fell 2.9% in 2010."

Now, that original post didn't differentiate between life and other insurance products available through these kinds of arrangements, but at least some of these numbers reflect life insurance sales.

Now there's even more bad news, and this is specifically related to payroll deduction (worksite marketed) life insurance:

"Middle-aged white Americans without four-year degrees are at increasing risk of dying [prematurely]."

There are, of course, any number of possible explanations for this, but Bloomberg's Jeanna Smialek puts the blame on drug and alcohol abuse, and "slowing progress against heart disease and cancer."

I'm not quite in agreement on this: after all, black men (and white women) face the same challenges, and I don't see evidence cited that they're dying any earlier. And this is drivel:

"For all the debate over whether college is worthwhile, high school graduates who go straight into the workforce have higher unemployment [and] weaker wage growth" than their college-educated peers.

Really?

They also have zero college debt, and at least least 4 years of wage-earning over their college-educated peers. And if they're in the trades, the odds are pretty good that they're going to earn more - perhaps a lot more - than the barrista with the 6 year feminist studies degree.

Something to consider.

Friday, April 21, 2017

"Is this covered by my dental plan?"

Fair question:

"[H]e performed a tooth extraction while standing on a hoverboard"

Finally! An ICD 10 code I could not find.

[Hat Tip: Notorious MWR]

"[H]e performed a tooth extraction while standing on a hoverboard"

Finally! An ICD 10 code I could not find.

[Hat Tip: Notorious MWR]

Dogs & Fleas

Back in the day, the insurance industry went all-in on ObamaCare (after all, what's not to love about a law that requires citizens to buy one's product?). And it appeared to be kind of a no-brainer: rack up big losses? No problemmo, we'll backstop those with a

Back in the day, the insurance industry went all-in on ObamaCare (after all, what's not to love about a law that requires citizens to buy one's product?). And it appeared to be kind of a no-brainer: rack up big losses? No problemmo, we'll backstop those with a "A federal judge dealt a major blow to a health insurer's attempt to recoup millions of dollars" by rejecting the carrier's lawsuit against HHS accusing the agency of "failing to make good on its obligation to pay nearly $130 million under the ACA risk corridors program."

This shouldn't have come as a shock to BX, since the program has been notoriously underfunded for quite some time:

"In October 2015, HHS officials announced that the program had taken in only enough cash ... to pay about 16% of the amounts owed "

Sustainability!

FoIB Jeff M wonders what affect, if any, this will have on the carrier's plans to bonus its execs millions of dollars for last year's winning performance. I think we all know the answer to that.

Thursday, April 20, 2017

Another Agent Acting (VERY) Badly

This is so wrong, on so many levels:

"An insurance agent has been indicted by a grand jury after prosecutors say she scammed an elderly woman out of nearly $40,000 in cash and annuities."

The agent, Mary Hawkey, apparently convinced her elderly victim, who suffers from dementia, to hand over some $10,000 in cash and $30,000 of annuities. Unlike the case we discussed last month, the wayward agent doesn't seem to have sold her victim new annuities, going instead for the much simpler "cash it out and pocket the proceeds" technique.

And there's this:

"That's what I'm afraid of is that there's going to be other victims out there and other families that may not know" the victim's granddaughter said.

Let's hope they're able to recover at least a portion of this poor woman's life savings.

[Hat Tip: FoIB Marita M]

"An insurance agent has been indicted by a grand jury after prosecutors say she scammed an elderly woman out of nearly $40,000 in cash and annuities."

The agent, Mary Hawkey, apparently convinced her elderly victim, who suffers from dementia, to hand over some $10,000 in cash and $30,000 of annuities. Unlike the case we discussed last month, the wayward agent doesn't seem to have sold her victim new annuities, going instead for the much simpler "cash it out and pocket the proceeds" technique.

And there's this:

"That's what I'm afraid of is that there's going to be other victims out there and other families that may not know" the victim's granddaughter said.

Let's hope they're able to recover at least a portion of this poor woman's life savings.

[Hat Tip: FoIB Marita M]

Abbot & Costello do Health Wonkery

Brad Wright hosts this week's Health Wonk Review, with an eclectic assortment of interesting and provocative posts.

Wednesday, April 19, 2017

Preventive Care News

The folks at United Healthcare recently announced "New Preventive Breast Screening and Cardiovascular Disease Services." On the one hand, this is welcome news for UHC insureds who worry about these kinds of things. But I'm not quite so sanguine.

Here's why:

First, UHC doesn't pay for these services, its insureds do. And since the mammography benefit continues to be for women only, it is grossly unfair to men whose premiums help fund it but cannot benefit from it (despite over 2,000 new cases of male breast cancer each year).

Second, the cost of the service itself is about $65 (over and above the "free" regular screening), so why is this even something for insurance to be involved with? And we wonder why health insurance premiums continue to skyrocket.

And what, exactly, does the new "Cardiovascular Disease Services" actually cover?

"Screening and medications for cholesterol to help prevent cardiovascular disease."

Well first, isn't Lipitor (et al) already covered under the prescription drug benefit? Well, yes, but this new "enhancement" covers them at 100%. And what's the actual cost to the consumer?

Less than $12.

So I ask again, why is this even "a thing?"

Sigh.

Here's why:

First, UHC doesn't pay for these services, its insureds do. And since the mammography benefit continues to be for women only, it is grossly unfair to men whose premiums help fund it but cannot benefit from it (despite over 2,000 new cases of male breast cancer each year).

Second, the cost of the service itself is about $65 (over and above the "free" regular screening), so why is this even something for insurance to be involved with? And we wonder why health insurance premiums continue to skyrocket.

And what, exactly, does the new "Cardiovascular Disease Services" actually cover?

"Screening and medications for cholesterol to help prevent cardiovascular disease."

Well first, isn't Lipitor (et al) already covered under the prescription drug benefit? Well, yes, but this new "enhancement" covers them at 100%. And what's the actual cost to the consumer?

Less than $12.

So I ask again, why is this even "a thing?"

Sigh.

Tuesday, April 18, 2017

404Care.gov: Nothing new under the sun [UPDATED]

[Please scroll down for update]

We've been posting on the insecurity of the fabled Exchange site for a very long while; here, for example:

"Centers for Medicare & Medicaid Services (CMS) was using only weak security measures to protect a HealthCare.gov performance dashboard data warehouse"

Turns out, the Federales knew from pretty much Minute Zero that the site was a security sinkhole:

"Judicial Watch today ... records showing that the Obamacare website was launched despite serious concerns by its security testing contractor, Mitre Corporation, as well as internal executive-level apprehension about security."

No kidding?

Which is why I consistently warn folks to stay away from the site as best they can, and to register there only when and if they qualify for - and want to use - a subsidy. Even then, I recommend protection.

UPDATE: Just received in email from Humana:

"Humana will be implementing a new security log-on process to continue to protect your information. We recently completed the first phase of this update process with our captcha roll-out as an additional log-on step, providing even greater protection over your online information."

Private sector vs Public.

What's that word again? Oh, yeah: Accountability.

We've been posting on the insecurity of the fabled Exchange site for a very long while; here, for example:

"Centers for Medicare & Medicaid Services (CMS) was using only weak security measures to protect a HealthCare.gov performance dashboard data warehouse"

Turns out, the Federales knew from pretty much Minute Zero that the site was a security sinkhole:

"Judicial Watch today ... records showing that the Obamacare website was launched despite serious concerns by its security testing contractor, Mitre Corporation, as well as internal executive-level apprehension about security."

No kidding?

Which is why I consistently warn folks to stay away from the site as best they can, and to register there only when and if they qualify for - and want to use - a subsidy. Even then, I recommend protection.

UPDATE: Just received in email from Humana:

"Humana will be implementing a new security log-on process to continue to protect your information. We recently completed the first phase of this update process with our captcha roll-out as an additional log-on step, providing even greater protection over your online information."

Private sector vs Public.

What's that word again? Oh, yeah: Accountability.

Not my monkeys... [UPDATED]

[Please scroll down for update]

As regular readers know, I elected to "sit out" the past Open Enrollment season:

"Due to the significant changes carriers have made to their compensation schedules (aka commissions), I don’t believe that I can continue to offer the kind of comprehensive service to which I, and you, have become accustomed."

Of course, I'm far from the only agent to have pulled that particular trigger. And next year'scircus Open Enrollment season promises to be even more stressful:

"CMS Officially Shortens 2018 Individual Health Enrollment Period ... will move the end of the open enrollment period for 2018 individual major medical coverage to Dec. 15 [,2017], from Jan. 31, 2018."

Thus lopping off a month and-a-half, or roughly 50%.

I can see no way that could possibly go south.

(UPDATE) HEH: FoIB Holly R send us this relevant announcement from the D'Unh! Department:

"UnitedHealth beats earnings forecasts as it pulls out of Obamacare markets"

Imagine that.

As regular readers know, I elected to "sit out" the past Open Enrollment season:

"Due to the significant changes carriers have made to their compensation schedules (aka commissions), I don’t believe that I can continue to offer the kind of comprehensive service to which I, and you, have become accustomed."

Of course, I'm far from the only agent to have pulled that particular trigger. And next year's

"CMS Officially Shortens 2018 Individual Health Enrollment Period ... will move the end of the open enrollment period for 2018 individual major medical coverage to Dec. 15 [,2017], from Jan. 31, 2018."

Thus lopping off a month and-a-half, or roughly 50%.

I can see no way that could possibly go south.

(UPDATE) HEH: FoIB Holly R send us this relevant announcement from the D'Unh! Department:

"UnitedHealth beats earnings forecasts as it pulls out of Obamacare markets"

Imagine that.

Monday, April 17, 2017

Medicaid Expansion Costs

MIT and Harvard should be proud. Two of their most beloved health care economists, Jon Gruber and Benny Sommers, just wrote an earth shattering article detailing the impact of Medicaid expansion and spending at the state level.

Using data from the National Association of State Budget Officers they found that from 2010-2015 the impact on state funding for Medicaid expansion had no impact on state budgets. Further, they were also able to show that funding for other areas such as education and transportation didn't suffer from any funding reductions.

According to Gruber this research provides evidence that “Expansion is basically free.” He then went on to say “The main lesson is there’s no sort of big hidden cost of expanding Medicaid. What you see is what you get. You get free health insurance for your citizens.”

Of course they did Jon. Because for states who chose to participate in Medicaid expansion the federal government is funding 100% of the costs from 2014-2016.

Using data from the National Association of State Budget Officers they found that from 2010-2015 the impact on state funding for Medicaid expansion had no impact on state budgets. Further, they were also able to show that funding for other areas such as education and transportation didn't suffer from any funding reductions.

According to Gruber this research provides evidence that “Expansion is basically free.” He then went on to say “The main lesson is there’s no sort of big hidden cost of expanding Medicaid. What you see is what you get. You get free health insurance for your citizens.”

Of course they did Jon. Because for states who chose to participate in Medicaid expansion the federal government is funding 100% of the costs from 2014-2016.

Perfection as the Enemy: A Risky Tale

Recently, a client came to me looking for individual disability insurance. He's self-employed, which always makes this search a bit more challenging, but has been making a decent living at it for a while, so not an insurmountable challenge. As always, I had him complete a pre-screen form so that I could obtain accurate quotes based on his height, weight, health, and the like. He indicated that he took an acid reflux med, which isn't really a major stumbling block for DI.

So, we looked at some quotes and, once again, Illinois Mutual blew everyone else away with the occupation class upgrade and embedded benefits. We arranged for him to come into the office to complete the application.

As we went through the app, it became clear that he hadn't disclosed to me all that was ailing him but, to be fair, I understood why: he is under the regular care of a chiropractor, to whom he goes several times a month as a preventative measure. He doesn't have any specific back or spine issues, and he prefers to keep it that way.

The problem is that underwriters' alarm bells go off when they see regular chiropractic visits, and had he disclosed this on the pre-screen I might have been able to avoid what ended up happening:

I received a note from the underwriter that "there would be an exclusion of coverage for any injury to, disease or disorder of the back or spine, its muscles, ligaments, discs or nerve roots, fracture by trauma excepted."

He really didn't like that, and asked me to withdraw the application because "I do not want to continue with the application process if this is what they are going to exclude me for coverage on any back injuries. I could have a car accident and have broken vertebrae and they wont cover it."

When I notified the underwriter, she very graciously pointed out the importance of the last 4 words of that exclusion: "fracture by trauma excepted." So I reached out once more, pointing out that "it’s possible that you’re letting the perfect be the enemy of the good:

It’s true that they wouldn’t pay for some back-related disability, but OTOH, they’d pay for a heart attack or stroke or slipping on the ice, etc - all of the 100’s of other causes."

This is a very fine line to be walking; I have to respect my clients' wishes and I certainly don't want to be perceived as a "pushy salesman," but I also have a duty to my clients to do the best job I can for them. So I sent that email but decided that that was as far as I felt comfortable going.

Ultimately, he replied "I understand what you mean but I am going to pass on it. They are too much of a risk for me, too."

Understood, but I still think he made the wrong call.

So, we looked at some quotes and, once again, Illinois Mutual blew everyone else away with the occupation class upgrade and embedded benefits. We arranged for him to come into the office to complete the application.

As we went through the app, it became clear that he hadn't disclosed to me all that was ailing him but, to be fair, I understood why: he is under the regular care of a chiropractor, to whom he goes several times a month as a preventative measure. He doesn't have any specific back or spine issues, and he prefers to keep it that way.

The problem is that underwriters' alarm bells go off when they see regular chiropractic visits, and had he disclosed this on the pre-screen I might have been able to avoid what ended up happening:

I received a note from the underwriter that "there would be an exclusion of coverage for any injury to, disease or disorder of the back or spine, its muscles, ligaments, discs or nerve roots, fracture by trauma excepted."

He really didn't like that, and asked me to withdraw the application because "I do not want to continue with the application process if this is what they are going to exclude me for coverage on any back injuries. I could have a car accident and have broken vertebrae and they wont cover it."

When I notified the underwriter, she very graciously pointed out the importance of the last 4 words of that exclusion: "fracture by trauma excepted." So I reached out once more, pointing out that "it’s possible that you’re letting the perfect be the enemy of the good:

It’s true that they wouldn’t pay for some back-related disability, but OTOH, they’d pay for a heart attack or stroke or slipping on the ice, etc - all of the 100’s of other causes."

This is a very fine line to be walking; I have to respect my clients' wishes and I certainly don't want to be perceived as a "pushy salesman," but I also have a duty to my clients to do the best job I can for them. So I sent that email but decided that that was as far as I felt comfortable going.

Ultimately, he replied "I understand what you mean but I am going to pass on it. They are too much of a risk for me, too."

Understood, but I still think he made the wrong call.

Saturday, April 15, 2017

Easter Miracle?

Easter is traditionally celebrated by Christians to recognize the miracle of the resurrection of Jesus the Christ.

What is a miracle? Is it hocus-pocus or truly something supernatural? To some it can be either, but more often than not a miracle is something ordinary but yet unexpected.

One dictionary defines miracle as "a surprising and welcome event that is not explicable by natural or scientific laws and is therefore considered to be the work of a divine agency."

A dear friend who is deeply passionate about their faith says there are no such things as coincidences, but there are God-incidences. I tend to agree, although if truth be known, I am not always in touch with God and more often than not completely miss the small miracles that occur right before me.

Miracles come in big packages with neon signs and in small ways that may be missed until someone points it out. Each of us define and recognize miracles differently.

A few months ago both our adult children were traveling to the other side of the world, two different countries, traveling independently of the other. One was in Switzerland and the Netherlands, the other in the China mainland. We prayed for their safety. Sure enough, they made it back without a hitch.

Was that a miracle? In spite of the fact the "odds" favored them returning home safely we chose to accept the miracle of their trips.

But for some people, in the last stages of life, a miracle can be as ordinary as watching the sun come up the next day.

What follows is a story of a miracle that is both ordinary and yet totally unexpected.

Is That All There Is?

Oliver Hart, age 11, knows his Bible stories. A few days ago, the school captain of Christ Church Grammar School in South Yarra (Australia) helped re-enact the Easter story - there were the 30 pieces of silver, the crown of thorns, the Crucifixion and resurrection.

The school says many of its parents aren't even believers, but they still want their children to know the critical stories of the Bible. As for 11 year old Oliver, "Easter symbolizes there is always hope … you don't have to believe in God, but I think the message in the story is a good one''.

Prime Minister Julia Gillard would agree. An atheist, Ms Gillard believes Australians need to understand the Bible because it ''has formed such an important part of our culture''.

Yet Oliver Hart is in a minority. Ms Gillard may have learned to recite scripture at her Baptist Sunday school, but many young Australians have no clue about the Good Samaritan, the Great Flood or even Easter. When Jesus went into the Garden of Gethsemane and prayed to God that he might be spared the horror of the cross, he might well have added that ''by 2011, most kids won't even know who I am … they'll be more concerned about why chocolate eggs are delivered by a rabbit''.

Many Adults are Equally Ambivalent About Christianity.

A psychologist who writes poetry and fiction, has reconsidered the Bible's value as a store of ''rich and beautiful language and evocative imagery''.

''The story of the Good Samaritan, and the many instances of Jesus challenging the cruel orthodoxies of the time, were good and powerful stories.''

But is that all they are? Good stories that might as well be fiction for all they know.

Bible stories about children, especially about the baby Jesus, still have resonance in the non-church community.

Jesus is The Problem

''It's the adult Jesus story that's in trouble,'' Professor Carroll says. ''The story of Good Friday and resurrection is floundering badly. If we lose the tragic Jesus story from the culture, we lose a lot. That symbol of the cross sits on top of Western civilization.''

He says the loss of biblical stories from the culture is a direct failing of the Christian churches, who have a responsibility to ''tell those stories in a way that is engaging today''.

In essence, Prof. Carroll is saying the stories don't capture our attention and draw us in, literally and figuratively, to the story of Jesus' life and death. In this short attention span world, the Easter story, the TRUE Easter story just doesn't resonate in today's glitzy, fast paced world.

In other words, it would take a MIRACLE to capture the attention of adults and children, compel them to set aside their electronic devices and unplug their ear buds, and listen to a history lesson about faith.

Are Moral Lessons Enough?

For the non-religious, stories that impart moral lessons are more appealing if they avoid religious overtones.

Amanda Cox, 38, a mother of three boys, gave up Sunday school for swimming club. ''The way they told the stories was boring,'' she says. And although Ms Cox found the religious angles ''off-putting'', she is sad the stories with their ''fantastic morals and lessons'' aren't as prevalent now.

As one raised in a family that attended church regularly, I can still recall being fascinated by the stories taught to us in Sunday School. It never occurred to me that building an ark that would hold all the animals as well as family members was a humanly impossible task. Or that Moses could wave a stick over the Red Sea and the waters would part so the Israelite's could escape Pharaoh's army. I did wonder why Jesus, who had done nothing wrong, arrested and crucified. Why would they do that to a man who had helped so many people?

One person suggested ''I do agree that some of the stories display great interpretation of good values, but the same thing could be said about Aesop's fables or even Shakespeare.''

Is that all that the Christian faith has to offer these days? Stories with good moral values?

Who Has Made a Lasting Impression in History?

Sadly for many that is true. I heard someone say that Jesus was a good man but so was Dr. Albert Schweitzer.

But did Dr. Schweitzer perform miracles that cannot be explained in human terms?

No doubt, Dr. Schweitzer made great contributions to the world and awarded a Nobel prize, but how many people today know what he did, or even know his name?

This Sunday many will attend church for the first time in months, or even years. Their motivations for attending on this particular day are varied. Some may attend out of obligation. Others may come to take their kids. Some will come hoping to reconnect with their faith.

Still others will attend, and never come back because the church was too crowded.

Whether you worship in a corporate setting or privately in your home, take a moment to reconnect with your past. Reflect on all that has happened in your life and how, through it all, you have had a good life so far. Maybe not perfect. Perhaps not the way you wanted, but you had a good life overall.

And maybe, just maybe, that is your miracle.

What is a miracle? Is it hocus-pocus or truly something supernatural? To some it can be either, but more often than not a miracle is something ordinary but yet unexpected.

One dictionary defines miracle as "a surprising and welcome event that is not explicable by natural or scientific laws and is therefore considered to be the work of a divine agency."

A dear friend who is deeply passionate about their faith says there are no such things as coincidences, but there are God-incidences. I tend to agree, although if truth be known, I am not always in touch with God and more often than not completely miss the small miracles that occur right before me.

Miracles come in big packages with neon signs and in small ways that may be missed until someone points it out. Each of us define and recognize miracles differently.

A few months ago both our adult children were traveling to the other side of the world, two different countries, traveling independently of the other. One was in Switzerland and the Netherlands, the other in the China mainland. We prayed for their safety. Sure enough, they made it back without a hitch.

Was that a miracle? In spite of the fact the "odds" favored them returning home safely we chose to accept the miracle of their trips.

But for some people, in the last stages of life, a miracle can be as ordinary as watching the sun come up the next day.

What follows is a story of a miracle that is both ordinary and yet totally unexpected.

Is That All There Is?

Oliver Hart, age 11, knows his Bible stories. A few days ago, the school captain of Christ Church Grammar School in South Yarra (Australia) helped re-enact the Easter story - there were the 30 pieces of silver, the crown of thorns, the Crucifixion and resurrection.

The school says many of its parents aren't even believers, but they still want their children to know the critical stories of the Bible. As for 11 year old Oliver, "Easter symbolizes there is always hope … you don't have to believe in God, but I think the message in the story is a good one''.

Prime Minister Julia Gillard would agree. An atheist, Ms Gillard believes Australians need to understand the Bible because it ''has formed such an important part of our culture''.

Yet Oliver Hart is in a minority. Ms Gillard may have learned to recite scripture at her Baptist Sunday school, but many young Australians have no clue about the Good Samaritan, the Great Flood or even Easter. When Jesus went into the Garden of Gethsemane and prayed to God that he might be spared the horror of the cross, he might well have added that ''by 2011, most kids won't even know who I am … they'll be more concerned about why chocolate eggs are delivered by a rabbit''.

Many Adults are Equally Ambivalent About Christianity.

A psychologist who writes poetry and fiction, has reconsidered the Bible's value as a store of ''rich and beautiful language and evocative imagery''.

''The story of the Good Samaritan, and the many instances of Jesus challenging the cruel orthodoxies of the time, were good and powerful stories.''

But is that all they are? Good stories that might as well be fiction for all they know.

Bible stories about children, especially about the baby Jesus, still have resonance in the non-church community.

Jesus is The Problem

''It's the adult Jesus story that's in trouble,'' Professor Carroll says. ''The story of Good Friday and resurrection is floundering badly. If we lose the tragic Jesus story from the culture, we lose a lot. That symbol of the cross sits on top of Western civilization.''

He says the loss of biblical stories from the culture is a direct failing of the Christian churches, who have a responsibility to ''tell those stories in a way that is engaging today''.

In essence, Prof. Carroll is saying the stories don't capture our attention and draw us in, literally and figuratively, to the story of Jesus' life and death. In this short attention span world, the Easter story, the TRUE Easter story just doesn't resonate in today's glitzy, fast paced world.

In other words, it would take a MIRACLE to capture the attention of adults and children, compel them to set aside their electronic devices and unplug their ear buds, and listen to a history lesson about faith.

Are Moral Lessons Enough?

For the non-religious, stories that impart moral lessons are more appealing if they avoid religious overtones.

Amanda Cox, 38, a mother of three boys, gave up Sunday school for swimming club. ''The way they told the stories was boring,'' she says. And although Ms Cox found the religious angles ''off-putting'', she is sad the stories with their ''fantastic morals and lessons'' aren't as prevalent now.

As one raised in a family that attended church regularly, I can still recall being fascinated by the stories taught to us in Sunday School. It never occurred to me that building an ark that would hold all the animals as well as family members was a humanly impossible task. Or that Moses could wave a stick over the Red Sea and the waters would part so the Israelite's could escape Pharaoh's army. I did wonder why Jesus, who had done nothing wrong, arrested and crucified. Why would they do that to a man who had helped so many people?

One person suggested ''I do agree that some of the stories display great interpretation of good values, but the same thing could be said about Aesop's fables or even Shakespeare.''

Is that all that the Christian faith has to offer these days? Stories with good moral values?

Who Has Made a Lasting Impression in History?

Sadly for many that is true. I heard someone say that Jesus was a good man but so was Dr. Albert Schweitzer.

But did Dr. Schweitzer perform miracles that cannot be explained in human terms?

No doubt, Dr. Schweitzer made great contributions to the world and awarded a Nobel prize, but how many people today know what he did, or even know his name?

This Sunday many will attend church for the first time in months, or even years. Their motivations for attending on this particular day are varied. Some may attend out of obligation. Others may come to take their kids. Some will come hoping to reconnect with their faith.

Still others will attend, and never come back because the church was too crowded.

Whether you worship in a corporate setting or privately in your home, take a moment to reconnect with your past. Reflect on all that has happened in your life and how, through it all, you have had a good life so far. Maybe not perfect. Perhaps not the way you wanted, but you had a good life overall.

And maybe, just maybe, that is your miracle.

Friday, April 14, 2017

Deadly Big Brother, MVNHS©-style

Young and old, government-run health "care" schemes are getting pretty good at reining in the cost of care. Last month, for example, we learned how the Dutch manage such a feat:

"A Dutch woman doctor who asked an elderly patient’s family to hold her down while she administered a fatal drug dose has been cleared under Holland’s euthanasia laws"

But hey, that's just a sick old woman. No way this would happen to a youngling.

Right?

Um:

"Doctors can withdraw life support from a sick baby with a rare genetic condition against his parents' wishes"

Apparently, It takes a village to kill a child.

But wait, it gets even better (for certain values of "better"):

"His parents ... had wanted to take him to the US for a treatment trial."

Of course, this is far from the first time we've blogged on the Much Vaunted National Health System©'s war on children:

"A mother has described how her baby was left to die 'like an abandoned animal' after hospital doctors repeatedly ignored her desperate pleas for help."

Which begs the question: how, exactly, are our Cousins Across the Pond going to pay for care, since they keep killing off their young 'uns?

"A Dutch woman doctor who asked an elderly patient’s family to hold her down while she administered a fatal drug dose has been cleared under Holland’s euthanasia laws"

But hey, that's just a sick old woman. No way this would happen to a youngling.

Right?

Um:

"Doctors can withdraw life support from a sick baby with a rare genetic condition against his parents' wishes"

Apparently, It takes a village to kill a child.

But wait, it gets even better (for certain values of "better"):

"His parents ... had wanted to take him to the US for a treatment trial."

Of course, this is far from the first time we've blogged on the Much Vaunted National Health System©'s war on children:

"A mother has described how her baby was left to die 'like an abandoned animal' after hospital doctors repeatedly ignored her desperate pleas for help."

Which begs the question: how, exactly, are our Cousins Across the Pond going to pay for care, since they keep killing off their young 'uns?

Twisting in the Wind

So, yesterday I fielded a call from a young lady looking for health insurance help. It seems that she travels quite a bit all over the country, and is having a very interesting (well, to me; problematic for her) issue:

She and her husband had been covered under his employer's plan, but that's gone away (I inferred that he'd been let go, but didn't pursue since I didn't need to know). She's been searching for replacement coverage herself, and is running out of time (they have but 5 days left on the Special Open Enrollment eligibility). The problem is that she needs a plan that will cover her while she's on the road.

Sorry, Charlie!

As we've mentioned, plans used be built on the PPO model, which offered (reduced) out-of-network coverage. Now (at least in this market) the only plans available are built on the HMO chassis, which basically covers out-of-network charges only for life-threatening emergency care.

So, get sick in Dayton, no problem.

Get sick in Milwaukee, problem.

I did tell her her that there are options:

First, Short Term Medical plans. These are still PPO-based, so she'd have coverage wherever she traveled in this great land of ours. But, they aren't ACA-compliant, and she can only keep a plan for 3 months at a time. And, of course, they don't cover any pre-exisiting conditions.

Second, I mentioned Dave's plan.

And third, I brought up Sharing Ministries.

She demurred on all three.

I did tell her I'd be happy to answer any other questions if she wants to cal back, but reminded her that the clock is ticking....

She and her husband had been covered under his employer's plan, but that's gone away (I inferred that he'd been let go, but didn't pursue since I didn't need to know). She's been searching for replacement coverage herself, and is running out of time (they have but 5 days left on the Special Open Enrollment eligibility). The problem is that she needs a plan that will cover her while she's on the road.

Sorry, Charlie!

As we've mentioned, plans used be built on the PPO model, which offered (reduced) out-of-network coverage. Now (at least in this market) the only plans available are built on the HMO chassis, which basically covers out-of-network charges only for life-threatening emergency care.

So, get sick in Dayton, no problem.

Get sick in Milwaukee, problem.

I did tell her her that there are options:

First, Short Term Medical plans. These are still PPO-based, so she'd have coverage wherever she traveled in this great land of ours. But, they aren't ACA-compliant, and she can only keep a plan for 3 months at a time. And, of course, they don't cover any pre-exisiting conditions.

Second, I mentioned Dave's plan.

And third, I brought up Sharing Ministries.

She demurred on all three.

I did tell her I'd be happy to answer any other questions if she wants to cal back, but reminded her that the clock is ticking....

Thursday, April 13, 2017

1035in' along

A few months ago, I called out Erie Insurance for what I considered inappropriate activity. Today, I received the final notice from our carrier's Home Office that the plan had, in fact, been surrendered, and the check cut and sent to Erie via 1035 exchange.

That's nice, Henry, but what the heck's a 1035 exchange? An exit off I-75?

No, it's actually a very useful tool we use to avoid excess taxation when trading life insurance polices. And I was quite surprised to find that, 12+ years in, we've never blogged on this.

Allow me to correct that:

First, we need to understand that in permanent life insurance plans (such as Whole or Universal Life), the cash value accumulates with no taxes due. It's called tax-deferred, but not tax-free: the funds accumulate until they're withdrawn, and then one is taxed on the gain over the premiums paid. Turns out, Marcus had paid almost $33,000 in premiums, and the policy value at time of surrender was just north of $87,000. So, he had a gain of about $54,000. If he had just cashed the policy out, and then sent the check over to Erie, he would be on the hook for taxes on that $54,000.

By using a 1035 exchange, and having the original carrier transfer the funds directly to (in this case) Erie, Marcus was saved a major hurtin'. I'm still of the opinion that this was (at best) ill-advised, but at least the gentleman was spared further damage.

That's nice, Henry, but what the heck's a 1035 exchange? An exit off I-75?

No, it's actually a very useful tool we use to avoid excess taxation when trading life insurance polices. And I was quite surprised to find that, 12+ years in, we've never blogged on this.

Allow me to correct that:

First, we need to understand that in permanent life insurance plans (such as Whole or Universal Life), the cash value accumulates with no taxes due. It's called tax-deferred, but not tax-free: the funds accumulate until they're withdrawn, and then one is taxed on the gain over the premiums paid. Turns out, Marcus had paid almost $33,000 in premiums, and the policy value at time of surrender was just north of $87,000. So, he had a gain of about $54,000. If he had just cashed the policy out, and then sent the check over to Erie, he would be on the hook for taxes on that $54,000.

By using a 1035 exchange, and having the original carrier transfer the funds directly to (in this case) Erie, Marcus was saved a major hurtin'. I'm still of the opinion that this was (at best) ill-advised, but at least the gentleman was spared further damage.

Wednesday, April 12, 2017

What does "across state lines" really mean?

I think the notion of buying insurance “across

state lines” is a misleading consumer cliché.

It misleads by suggesting that people who don’t live in the service area of the other state’s policy, would

need to travel to the other state to use their insurance. But that’s

not how it would work. The cliché is

misleading. Here's what I think.

I think we need more and

less-costly insurance choices in our OWN STATES.

I think to achieve that result, there’s

neither need nor logic for buying insurance in another state i.e., “across state

lines”. That’s because state lines are not the obstacles - state insurance

coverage mandates are the obstacles.

States generally require that each

insurance policy sold to its residents include all of that state’s insurance

mandates. Some states mandate much more coverage

than other states. That means the residents of those states have no choice:

they must buy more coverage than residents of other states. That’s a problem because buying more coverage

means they pay higher premiums. And

there’s nothing they can do about it.

Example. Alabama requires fewer mandates than

Connecticut. But Connecticut does not permit sale of a policy that contains

only Alabama mandates. Connecticut

residents would pay less premium for a policy that contains only Alabama

mandates. But they can’t buy it.

The Supreme Court ruled in the 1940’s

that the business of insurance is interstate.

Many federal insurance laws

derive their authority from the interstate nature of insurance – e.g., ERISA

and Obamacare. Nevertheless every state still

runs a kind of intrastate, legal monopoly over insurance by the use of mandates

unique to their state.

My

suggestion: modify federal law to

require that the coverage in ANY policy approved in ANY state, be available for

purchase in EVERY state. This

WOULD require the states abandon their monopolistic mandate regulations. It WOULD bring the possibility of some

premium relief to consumers in states that have the most mandates. It WOULD allow

insurers to sell lesser coverage than present state mandates allow, where they

already have service area networks. It

WOULD still allow the option of higher-coverage policies

everywhere. But it WOULD NOT require everyone

have identical basic coverage – as Obamacare does. It WOULD NOT require any insurance company to

build a new network anywhere so its policyholders could be in the service area.

And it WOULD NOT require anyone to

travel to another state to obtain medical treatment.

Is this a radical idea? I think not. Drivers’

licenses are accepted in every state. So are medical licenses, marriage

licenses, etc., etc. I believe there’s no good reason to keep state insurance

mandates. These mandates trap Americans

inside legalized state monopolies and oblige residents of some states to pay

higher premiums than residents of other states, for coverage they may not even want

to buy.

Why worry about all this now? After

all, Obamacare itself mandates a long list of “essential” coverages that every

policy must include. Those federal mandates

have narrowed coverage differences arising from state mandates. So what’s the problem? Well . . . Obamacare continues to

self-destruct. At some point, federally-mandated

essential coverages may end. At that

point, the choice and cost problems of state-specific coverage mandates return

– unless we think of a way to avoid them.

Let’s also keep in mind that this discussion is about medical insurance, not medical care. The cost of medical care is by far the biggest factor in the cost of medical insurance. Purchasing a policy with lesser coverage reduces one’s insurance cost, but does not reduce the cost of medical care. Still, I think this idea is worth considering because it can reduce insurance cost for many people; and it would do this by giving everyone more choices.

Let’s also keep in mind that this discussion is about medical insurance, not medical care. The cost of medical care is by far the biggest factor in the cost of medical insurance. Purchasing a policy with lesser coverage reduces one’s insurance cost, but does not reduce the cost of medical care. Still, I think this idea is worth considering because it can reduce insurance cost for many people; and it would do this by giving everyone more choices.

Tuesday, April 11, 2017

A Face for Radio

So, I made my talk radio debut yesterday on the Chad Adams show (a North Carolina institution). Many thanks to FoIB Jeff M for facilitating this.

It was a lot of fun.

Here's the show (my segment begins at ~30:00):

It was a lot of fun.

Here's the show (my segment begins at ~30:00):

Monday, April 10, 2017

Part Time Disability?

Got this from Illinos Mutual the other day, thought readers might find it interesting:

"Do all your Disability Income Insurance (DI) clients or prospects work full time? Probably not."

I've never really thought about it, but part time folks might consider disability insurance a good idea. For example, many (most?) part-timers are ineligible for company-sponsored short- or long-term disability plans. And they may not even know individual plans exist (after all, who's actively marketing to them?).

One caveat: when IM says part-time, they mean at least 20 hours a week (on average), so folks who work less than that aren't eligible. But I have to believe that there's a sizable group of folks who would fit into that over 20 but less than 40 hours demographic.

Something to consider, no?

"Do all your Disability Income Insurance (DI) clients or prospects work full time? Probably not."

I've never really thought about it, but part time folks might consider disability insurance a good idea. For example, many (most?) part-timers are ineligible for company-sponsored short- or long-term disability plans. And they may not even know individual plans exist (after all, who's actively marketing to them?).

One caveat: when IM says part-time, they mean at least 20 hours a week (on average), so folks who work less than that aren't eligible. But I have to believe that there's a sizable group of folks who would fit into that over 20 but less than 40 hours demographic.

Something to consider, no?

Friday, April 07, 2017

And Then There Was One

Remember this Golden Oldie:

As we continue to watch the (increasingly not slow-mo) implosion of ObamaCare, there's news, and then there's news that's kind of under the radar.

First the news (about which I'm sure most of our readers already know):

Wellmark is signalling that they'll follow Aetna out of the Hawkeye State:

"Wellmark Blue Cross and Blue Shield will no longer sell new individual health insurance policies in Iowa and some Iowans who have Wellmark insurance will lose it in 2018."

Which means that, in a few months, it's likely that Iowa's individual market will be down to exactly one carrier: Medica.

And just who is Medica?

Well, they're a regional carrier "offering health plans in Iowa, Minnesota, Nebraska, North Dakota, South Dakota and Wisconsin." Currently, they insure just shy of two million folks, but that includes all 6 states, and individual, group and Medicare plans.

Which raises some interesting questions:

Several months ago, we discussed "capacity;" that is, how much risk (how many clients) a given carrier is actually able to take on at any given time. The issue is no less critical here: is Medica going to be able to absorb all those new insureds?

And our friend Chad N offers this observation:

"Now Aetna is exiting Iowa’s Obamacare market. I believe that leaves only Medica who has been very non-committal about continuing (although I’d guess they will ask for a ridiculous premium increase and corner the market since HHS and the Iowa Insurance Division will have no other choice)."

Rock, meet hard place.

#ACAWinning!

As we continue to watch the (increasingly not slow-mo) implosion of ObamaCare, there's news, and then there's news that's kind of under the radar.

First the news (about which I'm sure most of our readers already know):

Wellmark is signalling that they'll follow Aetna out of the Hawkeye State:

"Wellmark Blue Cross and Blue Shield will no longer sell new individual health insurance policies in Iowa and some Iowans who have Wellmark insurance will lose it in 2018."

Which means that, in a few months, it's likely that Iowa's individual market will be down to exactly one carrier: Medica.

And just who is Medica?

Well, they're a regional carrier "offering health plans in Iowa, Minnesota, Nebraska, North Dakota, South Dakota and Wisconsin." Currently, they insure just shy of two million folks, but that includes all 6 states, and individual, group and Medicare plans.

Which raises some interesting questions:

Several months ago, we discussed "capacity;" that is, how much risk (how many clients) a given carrier is actually able to take on at any given time. The issue is no less critical here: is Medica going to be able to absorb all those new insureds?

And our friend Chad N offers this observation:

"Now Aetna is exiting Iowa’s Obamacare market. I believe that leaves only Medica who has been very non-committal about continuing (although I’d guess they will ask for a ridiculous premium increase and corner the market since HHS and the Iowa Insurance Division will have no other choice)."

Rock, meet hard place.

#ACAWinning!

Thursday, April 06, 2017

Once more unto the breach

/about/facepalmbear-5804f2af3df78cbc28913ff7.PNG)

Look, I've been a big fan of Direct Primary Care (DPC) and its cousin, Concierge medicine, for a very long time. But it is not a panacea. And under the ACA, it makes very little economic sense for most people.

Here's why:

On Twitter, Dr Matt McCord published a very cool graphic about the benefits of DPC. I replied that yes, the model does make financial sense for many providers, but not for most patients.

He replied "Not true in our growing High-deductible health care marketplace. Buy your own #healthcare fiduciary for $50/month."

And I responded "uh-hunh. Now do chemo."

To which the good doctor replied "A classic argument. Cancer, Trauma, Acute MI..these are not elective/preventative events. That is what Insurance is for."

Bingo.

Because that's the whole point: DPC doesn't provide for serious health issues (nor does it claim to, of course). That's up to the insurance. But under the ACA, plans must include most primary care already, so one is paying for it...twice.

How does this make financial sense?

And this is the issue I have with a number of DPC proponents: they're making the wrong argument. As long as ObamaCare remains the law of the land, there is never going to be a good economic rationale for DPC.

But there's a darned good health reason, and regular readers are already nodding their heads in agreement:

DPC guarantees quick access to care. It's why Britons, who have "free healthcare" willingly pay bigbucks pounds for the private version.

I wonder if/when our DPC friends will figure that out?

Here's why:

On Twitter, Dr Matt McCord published a very cool graphic about the benefits of DPC. I replied that yes, the model does make financial sense for many providers, but not for most patients.

He replied "Not true in our growing High-deductible health care marketplace. Buy your own #healthcare fiduciary for $50/month."

And I responded "uh-hunh. Now do chemo."

To which the good doctor replied "A classic argument. Cancer, Trauma, Acute MI..these are not elective/preventative events. That is what Insurance is for."

Bingo.

Because that's the whole point: DPC doesn't provide for serious health issues (nor does it claim to, of course). That's up to the insurance. But under the ACA, plans must include most primary care already, so one is paying for it...twice.

How does this make financial sense?

And this is the issue I have with a number of DPC proponents: they're making the wrong argument. As long as ObamaCare remains the law of the land, there is never going to be a good economic rationale for DPC.

But there's a darned good health reason, and regular readers are already nodding their heads in agreement:

DPC guarantees quick access to care. It's why Britons, who have "free healthcare" willingly pay big

I wonder if/when our DPC friends will figure that out?

Health Wonk Review: Pre-Passover edition

The Jewish holiday of Passover, which commemorates our freedom from years of slavery (among other things) begins next Monday evening. During the ceremony, we recite the 10 Plagues, and we actually have 10 great posts to offer, but I'm going to pass on linking posts and plagues.

Instead, I'm going to intersperse some interesting factoids about the celebration between entries. And please note that the factoids and the posts are not related:

■ On the seder plate displayed in the middle of the table, you'll find an egg, charoset (fruit and nut mixture), horseradish, greens, bitter herbs and the shankbone of a lamb.

Joe Paduda thinks it’s time to look to how ACA can be fixed, but doesn't see theRocket Surgeons Powers That Be in DC actually doing that. Instead, he's expecting Medicaid and Exchange de-funding, along with subtle efforts to add friction to enrollment and the individual markets. What a pollyanna 😃.

Instead, I'm going to intersperse some interesting factoids about the celebration between entries. And please note that the factoids and the posts are not related:

■ On the seder plate displayed in the middle of the table, you'll find an egg, charoset (fruit and nut mixture), horseradish, greens, bitter herbs and the shankbone of a lamb.

Joe Paduda thinks it’s time to look to how ACA can be fixed, but doesn't see the

■ Abraham

Lincoln Was Assassinated During Passover. According to the American

Jewish Historical Society, many Jews were in synagogue for the holiday

when news of Lincoln's assassination broke ... Sadly, a time that was

supposed to be full of celebration became one of mourning.

Good friend David Williams has an interesting podcast with the CEO of CleanSlate, which uses medication as part of its treatment approach to fighting opioid addiction.

Good friend David Williams has an interesting podcast with the CEO of CleanSlate, which uses medication as part of its treatment approach to fighting opioid addiction.

■ Matzah - unleavened bread - looks like a giant saltine. It's also the primary ingredient in "matzah brie" (fried matzah), a sort of Jewish French toast (and a particular favorite of your HWR host).

Uber wonk Roy Poses has a discussion on physician burnout with the CEOs of some big US hospital systems, including some of the most prestigious, and joined by the CEO of the American Medical Association.

Uber wonk Roy Poses has a discussion on physician burnout with the CEOs of some big US hospital systems, including some of the most prestigious, and joined by the CEO of the American Medical Association.

■ Four glasses of wine are consumed during the seder, all of which need to be Kosher for Passover. When I was growing up, this meant cough syrup Manischewitz or Mogen David. But in recent years, very tasty real wines have become available (I'm partial to the Merlots).

Our friend Brad Wright discusses his own interaction with our health care system as he recovers from a bout with Guillain-Barré Syndrome. It's quite eye-opening. R'fuah shleima, Brad.

On a happier note, he's also the proud papa of a beautiful bouncy baby girl (Mazel Tov!)

Our friend Brad Wright discusses his own interaction with our health care system as he recovers from a bout with Guillain-Barré Syndrome. It's quite eye-opening. R'fuah shleima, Brad.

On a happier note, he's also the proud papa of a beautiful bouncy baby girl (Mazel Tov!)

■ Libyan

Jews took Passover so seriously that the women ground flour for the

matzoh seven days ahead - wrapping scarves around their mouths and noses

so as not to contaminate the flour with their breath.

I imagine he's tired of hearing this, but Jason Shafrin continues to earn his keep as our favorite health care economist with posts like this week's, where he asks a seemingly innocent question: "Are physicians benevolent public servants or profit maximizers?" [I suggested he embrace the healing power of 'and']

I imagine he's tired of hearing this, but Jason Shafrin continues to earn his keep as our favorite health care economist with posts like this week's, where he asks a seemingly innocent question: "Are physicians benevolent public servants or profit maximizers?" [I suggested he embrace the healing power of 'and']

■ The seder is actually a service, complete with its own prayerbook, called a Haggaddah. There are an almost infinite variety of these available (I recently saw one based on the Harry Potter books).

Bradley Flansbaum's post actually ties up pretty neatly with Jason's. as he explores "The Great American Coding Swindle." AKA "How You, too, Can Game the System for Fun and Profit."

Bradley Flansbaum's post actually ties up pretty neatly with Jason's. as he explores "The Great American Coding Swindle." AKA "How You, too, Can Game the System for Fun and Profit."

■ In Afghanistan, a tradition of bopping each other on the noggin with green onions adds a festive air to the ceremony.

Our good friend Louise Norris, herself a veteran HWR hostess, offers us her take on clearing up some of the confusion over the ACA individual mandate penalty. Pretty timely, since tax day's less than a fortnight away.

Our good friend Louise Norris, herself a veteran HWR hostess, offers us her take on clearing up some of the confusion over the ACA individual mandate penalty. Pretty timely, since tax day's less than a fortnight away.

■ Syrian Jews have a custom of starting the storytelling aspect of the Haggadah by taking the matzah used during the Seder, placing it into a special bag resembling a knapsack, and throwing it over their shoulders. They then proceed to recite a verse in Hebrew about leaving the desert in haste.

And HWR co-founder (along with Joe Paduda above) Julie Ferguson sends along her colleague Tom Lynch's post on the impact the "Psychosocial Buzz" is having on timely Workers Comp payouts.

And HWR co-founder (along with Joe Paduda above) Julie Ferguson sends along her colleague Tom Lynch's post on the impact the "Psychosocial Buzz" is having on timely Workers Comp payouts.

■ A small container of salt water symbolizes the tears we shed as slaves, and into which we dip the greens.

Steve Anderson sends along Wendell Potter's response to RyanCare. Spoiler Alert: He's not a fan.

Steve Anderson sends along Wendell Potter's response to RyanCare. Spoiler Alert: He's not a fan.

■ Jews from Hungary like to bring the bling to their Passover meal by decorating their Seder table with gold and silver jewelry. The explanation offered for this custom is that the Israelites were given the precious metals by the Egyptians to hasten their exodus from the land.

Our own contribution this week is my post on a favorite golden oldie: price transparency in healthcare. Have we finally found my ideal (aka "The McDonald's Model")? Kinda looks that way (at least on a small scale).

Our own contribution this week is my post on a favorite golden oldie: price transparency in healthcare. Have we finally found my ideal (aka "The McDonald's Model")? Kinda looks that way (at least on a small scale).

Well, that's it for this edition. May you and your families enjoy a wonderful Passover and joyous Easter. And don't forget to join us on April 20th when Brad Wright hosts.

Subscribe to:

Posts (Atom)