Like Henry, I despair that our good politicians will never learn. Allowing carriers to rescind the legally mandated policy cancellations is an actuarial disaster.

Pricing in the exchanges is predicated on the assumption that healthy people are going to enroll along with the sick. If healthy people can keep a lower-cost plan, they will. The population in the guaranteed issued ACA compliant plans will have an even higher average claims level than originally projected.

Yes, it's for a limited period of time. But it's going to do major damage until things stabilize...and it's like hitting a bell every time you change the basic rules. It takes a long time before the vibrations die out.

Friday, November 15, 2013

In Video Veritas

Earlier this week, we reported that James O'Keefe's "Project Veritas" had uncovered abuses by the unvetted Navigators (as we'd predicted would happen). Lest one think that this was a "one off," isolated incident, Mr O is out today with another example (one suspects that he has a trove of these gems):

So between low turnout, increased risk of identity theft, and outright fraud, tell me again why this was such a great idea?

So between low turnout, increased risk of identity theft, and outright fraud, tell me again why this was such a great idea?

Thursday, November 14, 2013

The Face of Stupid

Every so often someone says something so completely brainless you're left to wonder how they live day-to-day. The fact that so many of those people teach at places like MIT or have degrees from supposedly prestigious places of learning just shows how broken our education system is.

This is Jonathan Gruber

"The only way to end that discriminatory system is to bring everyone into the system and pay one fair price. That means that the genetic winners, the lottery winners who've been paying an artificially low price because of this discrimination now will have to pay more in return. And that, by my estimate, is about four million people. In return, we'll have a fixed system where over 30 million people will now for the first time be able to access fairly price and guaranteed health insurance."

I just don't believe it's possible for someone that educated to say something so completely wrong. It's just not possible to spend that amount of time "learning" and be so ignorant.

4 million people underpay, which is suddenly enough for 30 million people to get insurance? That math don't equate. The 4 million would have to be underpaying by tens of thousands of dollars to subsidize 30 million people.

The claim that 30 million people will now for the first time be able to access fairly-priced and guaranteed insurance is ignorant. Only 4 million people didn't have insurance because they couldn't afford it or were denied. The other 40 million uninsured CHOSE not to buy it. I.e. the same 40 million that have not signed up under ObamaCare.

To be fair, he did say by his "estimate," so he hasn't lied, he is just an idiot that doesn't have the slightest idea what he is talking about.

"This law is really leaving those with employer insurance, those with government insurance alone."

Hum, I bet I could find tens of millions of people with employer insurance now paying $63 a year in new taxes, plus 2.4%, plus increased cost for mandatory benefits, etc etc who disagree.

How sheltered does someone have to be to say these things? Do they really believe it themselves? And what the heck are they teaching our kids?

And another fine mess...

_07.jpg)

What a difference a day makes:

"How can the government force carriers to re-file cancelled policy forms, and how do they handle the immediate problem that these plans are unlawful under the ObamaTax?"

Twenty-four hours later, we have our "answer:"

"President Barack Obama said Thursday that insurers will be able to continue health-insurance coverage next year for current policyholders"

Uh-hunh. Go on....

"The first caveat requires insurance companies to inform consumers of what their plans do not include"

Oh, well, that's simple then: just send out millions of additional confusing letters to policyholders already befuddled by the last round. One wonders how much the Post Office paid him to propose this.

And I'm sure that carriers will be jumping all over themselves to take on the additional burden of managing two completely different - and often contradictory - policy forms. Piece o'cake.

But wait, there's more!

"The second requires the insurance companies to inform consumers what they could get on the Obamacare marketplace, that they could qualify for tax credits or qualify for Medicaid."

That's right, let's use the private sector to pimp for more free health care, because Medicaid is so flush with cash as it is.

The 800-pound gorilla currently slobbering all over the dining room table, though, is how to square this particular circle:

"It's the law of the land" vice "hey, let's keep changing it willy-nilly."

Isn't that pretty much what got us here in the first place?

And because this whole exercise is giving me a headache, here's some appropriate mood music:

"How can the government force carriers to re-file cancelled policy forms, and how do they handle the immediate problem that these plans are unlawful under the ObamaTax?"

Twenty-four hours later, we have our "answer:"

"President Barack Obama said Thursday that insurers will be able to continue health-insurance coverage next year for current policyholders"

Uh-hunh. Go on....

"The first caveat requires insurance companies to inform consumers of what their plans do not include"

Oh, well, that's simple then: just send out millions of additional confusing letters to policyholders already befuddled by the last round. One wonders how much the Post Office paid him to propose this.

And I'm sure that carriers will be jumping all over themselves to take on the additional burden of managing two completely different - and often contradictory - policy forms. Piece o'cake.

But wait, there's more!

"The second requires the insurance companies to inform consumers what they could get on the Obamacare marketplace, that they could qualify for tax credits or qualify for Medicaid."

That's right, let's use the private sector to pimp for more free health care, because Medicaid is so flush with cash as it is.

The 800-pound gorilla currently slobbering all over the dining room table, though, is how to square this particular circle:

"It's the law of the land" vice "hey, let's keep changing it willy-nilly."

Isn't that pretty much what got us here in the first place?

And because this whole exercise is giving me a headache, here's some appropriate mood music:

Why Obamacare is Broken

The low information crowd is grasping at straws in an effort to defend the #trainwreck also known as #Obamacare. This exchange between Megyn Kelly and Dr. Ezekiel Emanuel is priceless . . . unless you buy into the lies that got us into this mess.

Go Megyn!

Go Megyn!

Wednesday, November 13, 2013

BREAKING: Rousing Success!

Do you recall the SNL skit a few weeks back? The one that (presciently) predicted that only 6 people would sign up?

Well guess who gets the last laugh, Lorne Michaels?

Wait, what?

No!

"Obama admin: Fewer than 27,000 signed up for health care using federal website."

And that includes folks who haven't actually bought anything, just have something "in the cart."

Ms Kathy must be so proud.

Well guess who gets the last laugh, Lorne Michaels?

Wait, what?

No!

"Obama admin: Fewer than 27,000 signed up for health care using federal website."

And that includes folks who haven't actually bought anything, just have something "in the cart."

Ms Kathy must be so proud.

[Hat Tip: Ace of Spades]

Toothpaste and the ObamaTax

It seems that Our Betters in Capital City never learn. Four years ago, they rammed through a piece of legislation with virtually no input from folks with actual industry experience. We've seen the results: "no, you can't keep your insurance."

Now various Congresscritters, in an effort to at least mitigate the damage wrought by that broken promise, are proposing bills to allow - or force - insurance companies to rescind all these cancellations.

The latest twist is in California, whose Insurance Commissioner has forced Blue Cross to delay 104,000 such cancellations to February.

Here's the problem with all of this:

It's one thing if an insurer erroneously cancels your policy: that can be fixed via a simple reinstatement form. But it's quite another thing when the insurer must cancel an entire policy form - that is, the actual block of business - because the Federal law has deemed it unacceptable ("substandard").

Here are the two primary challenges I see:

First, it puts state Insurance Commissioners in direct conflict with Federal law. This isn't a simple (and unlawful) waiver: it's a direct and explicit flaunting of ACA. In short, it pits the Supremacy Clause against the 10th Amendment. It will be, um, interesting to see how that plays out.

Second, and more critical, is a very simple question. Yesterday, Bob wrote about "the House supported "If you like your health care plan you can keep it" offering," to which I commented "How?" And that is the only question that really matters. How can the government force carriers to re-file cancelled policy forms, and how do they handle the immediate problem that these plans are unlawful under the ObamaTax?

I just don't see how they put that toothpaste back in the tube.

Now various Congresscritters, in an effort to at least mitigate the damage wrought by that broken promise, are proposing bills to allow - or force - insurance companies to rescind all these cancellations.

The latest twist is in California, whose Insurance Commissioner has forced Blue Cross to delay 104,000 such cancellations to February.

Here's the problem with all of this:

It's one thing if an insurer erroneously cancels your policy: that can be fixed via a simple reinstatement form. But it's quite another thing when the insurer must cancel an entire policy form - that is, the actual block of business - because the Federal law has deemed it unacceptable ("substandard").

Here are the two primary challenges I see:

First, it puts state Insurance Commissioners in direct conflict with Federal law. This isn't a simple (and unlawful) waiver: it's a direct and explicit flaunting of ACA. In short, it pits the Supremacy Clause against the 10th Amendment. It will be, um, interesting to see how that plays out.

Second, and more critical, is a very simple question. Yesterday, Bob wrote about "the House supported "If you like your health care plan you can keep it" offering," to which I commented "How?" And that is the only question that really matters. How can the government force carriers to re-file cancelled policy forms, and how do they handle the immediate problem that these plans are unlawful under the ObamaTax?

I just don't see how they put that toothpaste back in the tube.

Speaking of Presidential "misspeaking" . . .

President Obama's defenders claim he "misspoke" when he said "you can keep your insurance if you like it". They claim Obama really meant that you can keep the insurance you like . . . if you bought it before March 21, 2010 and if it meets HHS standards that were written after March 21, 2010.

Well, America now knows for a fact that Obama never said all that. As a result, most people now doubt Obama ever meant all that, either. Besides, how likely is it that the president "misspoke" more than 30 times on the record?

Well - surprise - that is not the only such incident.

During the campaign in 2007-2008, candidate Obama promised over and over that his health plan would "reduce the average family health care premiums by $2,500 a year."

Now in 2013 comes David Cutler--a respected economist - to tell us that in fact, Obama really, really, did assert that "his health-care reform plan would save $2,500 per family relative to the trends at the time.”

Get that? Relative to the trends at the time?

Did you miss that last part about trend in all those campaign promises? I sure did.

Seems to me that Candidate Obama and President Obama have behaved consistently for at least 6 years: first, make promises you know you cannot fulfill. Then count on academia, the media, and the low-information voters to cover for you by explaining you "misspoke" dozens of time and, besides, that you never said what you said.

O brave new world that hath such people in't!!

Well, America now knows for a fact that Obama never said all that. As a result, most people now doubt Obama ever meant all that, either. Besides, how likely is it that the president "misspoke" more than 30 times on the record?

Well - surprise - that is not the only such incident.

During the campaign in 2007-2008, candidate Obama promised over and over that his health plan would "reduce the average family health care premiums by $2,500 a year."

Now in 2013 comes David Cutler--a respected economist - to tell us that in fact, Obama really, really, did assert that "his health-care reform plan would save $2,500 per family relative to the trends at the time.”

Get that? Relative to the trends at the time?

Did you miss that last part about trend in all those campaign promises? I sure did.

Seems to me that Candidate Obama and President Obama have behaved consistently for at least 6 years: first, make promises you know you cannot fulfill. Then count on academia, the media, and the low-information voters to cover for you by explaining you "misspoke" dozens of time and, besides, that you never said what you said.

O brave new world that hath such people in't!!

ObamaTax Update: Non-Exchange Edition

Had enough news about the ongoing meshugas that is the Exchange?

Me, too. So, in a demonstration of civic spirit, here's some ObamaTax news that has nothing to do with the Exchanges:

■ We've warred with them, killed their leader and continue to keep them in a Cuban prison-camp, but that doesn't mean that we don't care about their health (check the article's headline for an explanation):

"Non-citizens are eligible for Medicaid and CHIP (Children’s Health Insurance Program) ... the documentation and verification process for such enrollments was significantly eased by regulations in the Affordable Care Act."

9/11? Never heard of it.

■ Some good news for folks who object to thebirth control convenience items mandate:

"In a 2-1 ruling on Friday, a federal appeals court in Chicago upheld the rights of both individuals and companies to challenge Obamacare's contraception-abortifacient-sterilization mandate."

We last discussed this case last December, proving once again that the wheels of justice grind ever-so-slowly.

■ Did you know that November is Long Term Care insurance awareness month? Well it is, and here's some interesting news from one of the players:

"Executives at Manulife Financial ... think the benefits of staying in the private long-term care insurance (LTCI) market outweigh the benefits of getting out."

That's good news for fans of competition, which tends to help drive prices down and quality up (generally speaking).

The bad news is that they're considering some substantial rate hikes:

"The average increase in the new round would be about 25 percent."

Yikes.

If you're on the fence about considering LTCi for yourself or a loved one, Herman Brun's excellent post on the topic has stood well the test of time.

Me, too. So, in a demonstration of civic spirit, here's some ObamaTax news that has nothing to do with the Exchanges:

■ We've warred with them, killed their leader and continue to keep them in a Cuban prison-camp, but that doesn't mean that we don't care about their health (check the article's headline for an explanation):

"Non-citizens are eligible for Medicaid and CHIP (Children’s Health Insurance Program) ... the documentation and verification process for such enrollments was significantly eased by regulations in the Affordable Care Act."

9/11? Never heard of it.

■ Some good news for folks who object to the

"In a 2-1 ruling on Friday, a federal appeals court in Chicago upheld the rights of both individuals and companies to challenge Obamacare's contraception-abortifacient-sterilization mandate."

We last discussed this case last December, proving once again that the wheels of justice grind ever-so-slowly.

■ Did you know that November is Long Term Care insurance awareness month? Well it is, and here's some interesting news from one of the players:

"Executives at Manulife Financial ... think the benefits of staying in the private long-term care insurance (LTCI) market outweigh the benefits of getting out."

That's good news for fans of competition, which tends to help drive prices down and quality up (generally speaking).

The bad news is that they're considering some substantial rate hikes:

"The average increase in the new round would be about 25 percent."

Yikes.

If you're on the fence about considering LTCi for yourself or a loved one, Herman Brun's excellent post on the topic has stood well the test of time.

Cavalcade of Risk #196: A Delicate Balance

Matt Becker makes his CavRisk hosting

debut with a tremendous collection of interesting posts and excellent

commentary on each one.

Thanks, Matt!

Thanks, Matt!

Tuesday, November 12, 2013

The Non-Apology and The Non-Solution

"If you like your health care plan, you can keep it. Period".

"If you like your health care plan, you can keep it. Period". That begat,

For those Americans who already have health insurance, the only changes you will see under the law are new benefits, better protections from insurance company abuses, and more value for every dollar you spend on health care. If you like your plan you can keep it and you don’t have to change a thing due to the health care law.Well, not quite true.

New benefits, higher premiums, higher out of pocket. But other than that . . .

And the latest iteration is,

“I am sorry that they, you know, are finding themselves in this situation, based on assurances they got from me.” Well, what situation is that, Mr. President? The situation that they can’t access the Obamacare exchanges. The president went on to say, “Keep in mind that most of the folks who got these cancellation letters, they’ll be able to get better care at the same cost or cheaper in these new marketplaces. . . . The majority of folks will end up being better off, of course. Because the Web site’s not working right, they don’t necessarily know it.”Washington Post

Let's break this down.

"I am sorry they are finding themselves in this situation".So is he sorry he lied to the people and got caught telling a whopper? Kind of sounds like it.

most of the folks who got these cancellation letters, they’ll be able to get better care at the same cost or cheaper in these new marketplaces.Cheaper, but only if they qualify for a subsidy.

And perhaps that is what Jay Carney, the official weasel for the administration, meant when he said this.

“It is certainly the belief of the drafters of the law and the President that one of the purposes here is to set some minimum standards for coverage so that every American who gets insurance coverage has some security and certainty about the benefits they’re going to receive.”Most seem to think there will be a partial repeal of the law, or maybe even an amendment such as the House supported "If you like your health care plan you can keep it" offering.

But neither Carney nor El Prez said anything about keeping your plan, only that you deserved something better than the "inferior" insurance policies currently being sold.

So what is the grand solution?

Create a new subsidy class.

If you lost your inferior insurance you can keep your new #Obamacare plan and the government will help you pay for it.

Problem solved and DC has created a whole new group of entitlement addicts.

I think James Carville is right. #Obama needs to take a few hits off a crack pipe.

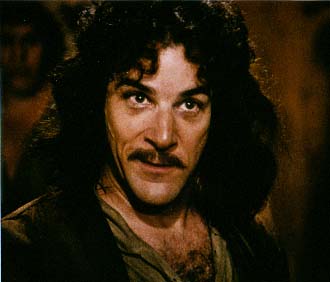

Inigo Montoya and the ObamaTax Exchange

In the classic film "The Princess Bride," Mandy Patinkin's character is dubious of another character's understanding of a rather common term ("inconceivable!"). He famously observes: "You keep using that word. I dunna think it means what you think it means."

Here's a great example, ripped from today's headlines:

"Medicaid signups an early Obamacare bright spot ... Medicaid has signed up 444,000 people in 10 states in the six weeks since open enrollment began"

Um, Kathy? That's not a "success," that's a major fail.

Why?

Medicaid enrollees are a net drain on the system from the moment they sign up. By definition, they pay no premiums, but have full access to health care, including pre-existing conditions, even maternity. They are the exact opposite of what the ObamaTax needs to survive (let alone thrive).

Thus far, less than 50,000 actual, paying customers have signed up. Of those, at least some - and probably most - will be eligible for subsidies, and have pre-existing conditions. But let's say they're all in Olympic shape. That's almost 10 Medicaid enrollees for every Exchange "buyer."

Sustainability. I dunna think it means what Ms Shecantbeserious thinks it means.

Here's a great example, ripped from today's headlines:

"Medicaid signups an early Obamacare bright spot ... Medicaid has signed up 444,000 people in 10 states in the six weeks since open enrollment began"

Um, Kathy? That's not a "success," that's a major fail.

Why?

Medicaid enrollees are a net drain on the system from the moment they sign up. By definition, they pay no premiums, but have full access to health care, including pre-existing conditions, even maternity. They are the exact opposite of what the ObamaTax needs to survive (let alone thrive).

Thus far, less than 50,000 actual, paying customers have signed up. Of those, at least some - and probably most - will be eligible for subsidies, and have pre-existing conditions. But let's say they're all in Olympic shape. That's almost 10 Medicaid enrollees for every Exchange "buyer."

Sustainability. I dunna think it means what Ms Shecantbeserious thinks it means.

More Agents? Heh. [UPDATED & BUMPED]

"[HHS Secretary Shecantbeserious] wants “to bring 60,000 more” agents and brokers on for consumer assistance with the [ObamaTax] federally run exchanges."

I bet.

Apparently, some 70,000 of us have already completed the FFM Certification process. It's unclear how many "health insurance agents" are out there, but it seems to be in the hundreds of thousands. And of course, we're trained to actually help clients make informed decisions, and vetted for knowledge and honesty.

Unlike some.

UPDATE: Yeah, those unlicensed, unvetted Navigators are working out so well. And at a paltry $67 million (so far) yet:

"Government-paid workers supposedly trained to uphold the law advise clients on how to lie on government forms, evade legal requirements, and ignore proper procedures ... The investigator then poses as a low-income worker at a university who has unreported cash income on the side, worrying about how that might affect his premium subsidies"

Of course the taxpayer-funded Navigator advises the would-be tax-evader and subsidy-cheat to do the right thing and decalre the income.

Right?

Not so much:

"Yeah, it didn’t happen,” another navigator says. One more chimes in: “Never report it.”

Here's the stomach-turning video:

I bet.

Apparently, some 70,000 of us have already completed the FFM Certification process. It's unclear how many "health insurance agents" are out there, but it seems to be in the hundreds of thousands. And of course, we're trained to actually help clients make informed decisions, and vetted for knowledge and honesty.

Unlike some.

UPDATE: Yeah, those unlicensed, unvetted Navigators are working out so well. And at a paltry $67 million (so far) yet:

"Government-paid workers supposedly trained to uphold the law advise clients on how to lie on government forms, evade legal requirements, and ignore proper procedures ... The investigator then poses as a low-income worker at a university who has unreported cash income on the side, worrying about how that might affect his premium subsidies"

Of course the taxpayer-funded Navigator advises the would-be tax-evader and subsidy-cheat to do the right thing and decalre the income.

Right?

Not so much:

"Yeah, it didn’t happen,” another navigator says. One more chimes in: “Never report it.”

Here's the stomach-turning video:

Tech, Insurance, and HC.gov

For a while now, we've been using a service call FormFire to get competitive quotes for small group clients. Basically, the agent and the employer each sign up with the service, and each employee is given a secure sign-in to enter health and other information. Once that's collated, the agent advises the FormFire folks which carriers to quote. There's a nominal fee involved, which the agent foots.

That's the short story version, but one can imagine all the back-end requirements necessary to make this work: HIPAA and other privacy requirements, collation and verification of data, making sure the info is formatted correctly for each carrier, etc. And of course there's the front-end: ease of use for the would-be client is a must, and participating employees must also trust that their personal and financial info is secure.

Sounds familiar, no?

FormFire's CEO just published a piece on the company's blog sharing his perspective on the Exchangeroll-out train-wreck, and he speaks from authority:

"It may seem only natural now, but ten years ago – when I created what would eventually become FormFire – paper was still very much the only currency in use ... we’ve pushed, clawed and fought our way from tolerance to acceptance to being even the preferred way of working in the markets we serve."

Makes sense: bits beat scraps. But what lessons would Mr Epp have us - and by extension, our Betters in Capital City - draw from his successful private sector experience?

His Top 5 lists key items, from "Too many cooks in the kitchen" to "Lack of infrastructure planning." But don't be put off by the tech-talk: this post is easily accessible to anyone who's ever written an email or clicked a link.

Recommended.

That's the short story version, but one can imagine all the back-end requirements necessary to make this work: HIPAA and other privacy requirements, collation and verification of data, making sure the info is formatted correctly for each carrier, etc. And of course there's the front-end: ease of use for the would-be client is a must, and participating employees must also trust that their personal and financial info is secure.

Sounds familiar, no?

FormFire's CEO just published a piece on the company's blog sharing his perspective on the Exchange

"It may seem only natural now, but ten years ago – when I created what would eventually become FormFire – paper was still very much the only currency in use ... we’ve pushed, clawed and fought our way from tolerance to acceptance to being even the preferred way of working in the markets we serve."

Makes sense: bits beat scraps. But what lessons would Mr Epp have us - and by extension, our Betters in Capital City - draw from his successful private sector experience?

His Top 5 lists key items, from "Too many cooks in the kitchen" to "Lack of infrastructure planning." But don't be put off by the tech-talk: this post is easily accessible to anyone who's ever written an email or clicked a link.

Recommended.

The Shy Guy

Remember when you were in school and had a crush on a cute girl? You would hold her hand in the movies. Take her to the prom.

Remember when you were in school and had a crush on a cute girl? You would hold her hand in the movies. Take her to the prom.Except none of this ever happened.

Because you were too shy to ever tell her how you really felt about her. You had a dream, but never followed through.

#Obamacare is the same way.

“In the data that will be released this week, ‘enrollment’ will measure people who have filled out an application and selected a qualified health plan in the marketplace,” the official told the paper.

The distinction is an important one, following reports like the one last week in which the Senate Finance Committee showed that only five individuals had enrolled in the District of Columbia's insurance marketplace.

In fact, only five individuals had selected a plan and sent their first month's payment insurers. Most individuals appear to be waiting to mail in that check until it is due in December, as coverage won't begin until Jan. 1.

Enrollment = picking a plan.

Kind of like window shopping.

Monday, November 11, 2013

Lipstick. Pig. [UPDATED]

Some assembly required:

"States with functioning exchanges have signed up 49,100 people compared with the 1.4 million people expected to be enrolled for 2014"

Two Three things to note:

1 - This represents only those states with non-Fed-run Exchanges. Which then begs the question: how many (or, more precisely: few) have signed up at the one "run" by Ms Shecantbeserious?

and

2 -How many have "successfully enrolled" on fraudulent "Exchanges?"

and

3 - Of those who did sign up on the state Exchanges, how many were the young, healthy (and easily duped) needed to actually fund this train-wreck?

Inquiring minds want to know.

"States with functioning exchanges have signed up 49,100 people compared with the 1.4 million people expected to be enrolled for 2014"

1 - This represents only those states with non-Fed-run Exchanges. Which then begs the question: how many (or, more precisely: few) have signed up at the one "run" by Ms Shecantbeserious?

and

2 -How many have "successfully enrolled" on fraudulent "Exchanges?"

and

3 - Of those who did sign up on the state Exchanges, how many were the young, healthy (and easily duped) needed to actually fund this train-wreck?

Inquiring minds want to know.

How it's done

Hundreds of millions of dollars and 3+ years later, and Healthcare.gov still doesn't work. Perhaps one is thinking that's an unfair characterization, and that the task was well-nigh impossible to accomplish in that time-frame and budget.

One would be wrong:

"Ning Liang, George Kalogeropoulos and Michael Wasser developed a site in matter of days – and it does things the expensive and faltering healthcare.gov can’t do."

Ah, but they must be long-time coding veterans with decades of experience on which to rely, and mega-donors willing to fund them.

Um, not so much:

"... the three 20-year-olds say they worked on the project as a service rather than to make money."

Kids these days.

[Hat Tip: FoIB "Dez"]

One would be wrong:

"Ning Liang, George Kalogeropoulos and Michael Wasser developed a site in matter of days – and it does things the expensive and faltering healthcare.gov can’t do."

Ah, but they must be long-time coding veterans with decades of experience on which to rely, and mega-donors willing to fund them.

Um, not so much:

"... the three 20-year-olds say they worked on the project as a service rather than to make money."

Kids these days.

[Hat Tip: FoIB "Dez"]

From the mailbag: Gaming the ObamaTax

We get mail!

Readers may recall Dr Stuart Fickler, a retired but not retiring physicist. During his career, Dr Fickler has been involved in research, education and high-tech business. He has received national recognition in the area of systems based Total Quality Management, and has led successful efforts in improving manufacturing and educational systems.

Today, he writes:

Although I am very familiar with complex systems in general, I am not familiar with the practical application to the insurance industry. Therefore, I am requesting your expert opinion on the following.

It is well known that the more complex a system is, the more vulnerable it becomes to "gaming." By gaming, I mean the process of manipulating the system in a manner that would be detrimental to the users of the system. This manipulation can be external or internal. A familiar simple example of external manipulation is identity theft. An example of internal manipulation could be a system that is designed to achieve outcomes other than those stated to the user. An illustration of this might be a financial system that manipulates its fees and costs in a way that reduces earnings to investors.

It appears to me that a system as complex as Obamacare is vulnerable to a vast range of gaming. To be clear, I am not referring to just the computer aspects of the system, but the entire system, from applying to delivery of the care itself.

A simple example of this might be the following. Someone whose income meets the income requirements for Medicaid (about $15,000/year single, about $31,000/year family of four) and who is in reasonably good health might opt for the free care offered by that program. If, at a later time, that person is told by a physician that he/she might require a major medical procedure, that person can game the system. That is, if they don't want to take the risk of "second class medical treatment", they can switch over to the "marketplace" insurance. The result would be a considerable cost savings to the "gamer". On the other hand, this would add to the risk of the insurance pool, and additional cost to those who purchased the insurance in good faith.

Is this a feasible scenario in the present context of Obamacare? Also, can you and your colleagues think of other "games"? It might be useful to forewarn those who depend on your trust.

Thank-you,

Stuart Fickler, Ph.D.

Thanks, Dr Fickler, for a great question, and an interesting challenge. The major issue that jumps out at me is this:

"If, at a later time, that person is told by a physician that he/she might require a major medical procedure, that person can game the system ... they can switch over to the "marketplace" insurance."

I'm not convinced it'd be that easy: what if the diagnosis came, and treatment was scheduled to begin, between regularly scheduled Open Enrollment periods?

It's true that "[l]oss of minimum essential coverage" would trigger a Special Enrollment Period. But note how this is worded: "e.g., loss of Medicaid eligibility" [emphasis added]. It's not clear to me that unilaterally and voluntarily "quitting" Medicaid would be treated as "losing eligibility." I think that, at best, it would be treated as an "[o]ther exceptional circumstance" and require a review. Does someone with (say) Stage 4 cancer really want to voluntarily leave their fate in the hands of bureaucrats whose rules will likely look a lot likethe IPAB Death Panels?

On the other hand, I'm sure there are other ways for "bad actors" to take advantage of this complex, unwieldy system. I'll echo Dr Fickler's call for other possible examples. Have at it!

Readers may recall Dr Stuart Fickler, a retired but not retiring physicist. During his career, Dr Fickler has been involved in research, education and high-tech business. He has received national recognition in the area of systems based Total Quality Management, and has led successful efforts in improving manufacturing and educational systems.

Today, he writes:

Although I am very familiar with complex systems in general, I am not familiar with the practical application to the insurance industry. Therefore, I am requesting your expert opinion on the following.

It is well known that the more complex a system is, the more vulnerable it becomes to "gaming." By gaming, I mean the process of manipulating the system in a manner that would be detrimental to the users of the system. This manipulation can be external or internal. A familiar simple example of external manipulation is identity theft. An example of internal manipulation could be a system that is designed to achieve outcomes other than those stated to the user. An illustration of this might be a financial system that manipulates its fees and costs in a way that reduces earnings to investors.

It appears to me that a system as complex as Obamacare is vulnerable to a vast range of gaming. To be clear, I am not referring to just the computer aspects of the system, but the entire system, from applying to delivery of the care itself.

A simple example of this might be the following. Someone whose income meets the income requirements for Medicaid (about $15,000/year single, about $31,000/year family of four) and who is in reasonably good health might opt for the free care offered by that program. If, at a later time, that person is told by a physician that he/she might require a major medical procedure, that person can game the system. That is, if they don't want to take the risk of "second class medical treatment", they can switch over to the "marketplace" insurance. The result would be a considerable cost savings to the "gamer". On the other hand, this would add to the risk of the insurance pool, and additional cost to those who purchased the insurance in good faith.

Is this a feasible scenario in the present context of Obamacare? Also, can you and your colleagues think of other "games"? It might be useful to forewarn those who depend on your trust.

Thank-you,

Stuart Fickler, Ph.D.

Thanks, Dr Fickler, for a great question, and an interesting challenge. The major issue that jumps out at me is this:

"If, at a later time, that person is told by a physician that he/she might require a major medical procedure, that person can game the system ... they can switch over to the "marketplace" insurance."

I'm not convinced it'd be that easy: what if the diagnosis came, and treatment was scheduled to begin, between regularly scheduled Open Enrollment periods?

It's true that "[l]oss of minimum essential coverage" would trigger a Special Enrollment Period. But note how this is worded: "e.g., loss of Medicaid eligibility" [emphasis added]. It's not clear to me that unilaterally and voluntarily "quitting" Medicaid would be treated as "losing eligibility." I think that, at best, it would be treated as an "[o]ther exceptional circumstance" and require a review. Does someone with (say) Stage 4 cancer really want to voluntarily leave their fate in the hands of bureaucrats whose rules will likely look a lot like

On the other hand, I'm sure there are other ways for "bad actors" to take advantage of this complex, unwieldy system. I'll echo Dr Fickler's call for other possible examples. Have at it!

Subscribe to:

Posts (Atom)